Question: Please show work for thumbs up:) Consider the bivariate VAR(1) process, where yt = (41,t, 42,t)': Yt ut Ayt-1 + ut WN(0, 0) 0.4 0.3

Please show work for thumbs up:)

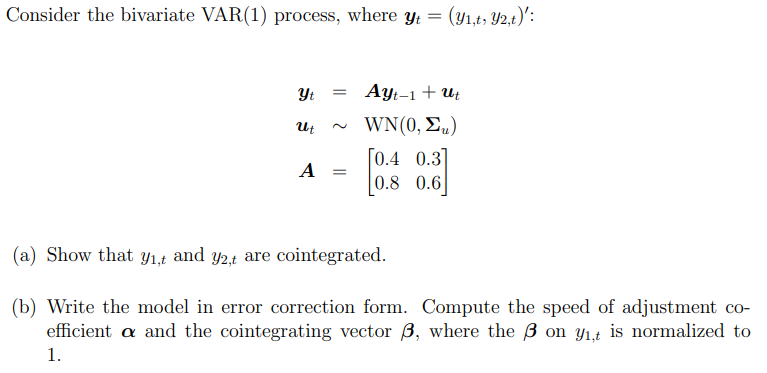

Consider the bivariate VAR(1) process, where yt = (41,t, 42,t)': Yt ut Ayt-1 + ut WN(0, 0) 0.4 0.3 0.8 0.6 A (a) Show that 41,4 and 42,4 are cointegrated. (b) Write the model in error correction form. Compute the speed of adjustment co- efficient a and the cointegrating vector , where the B on 41,t is normalized to 1. Consider the bivariate VAR(1) process, where yt = (41,t, 42,t)': Yt ut Ayt-1 + ut WN(0, 0) 0.4 0.3 0.8 0.6 A (a) Show that 41,4 and 42,4 are cointegrated. (b) Write the model in error correction form. Compute the speed of adjustment co- efficient a and the cointegrating vector , where the B on 41,t is normalized to 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts