Question: Please show work in excel for further understanding. Chap 7. Question 4: 1. Cray Researdi sold a super computer to the Max Planck Institute in

Please show work in excel for further understanding.

Chap 7. Question 4:

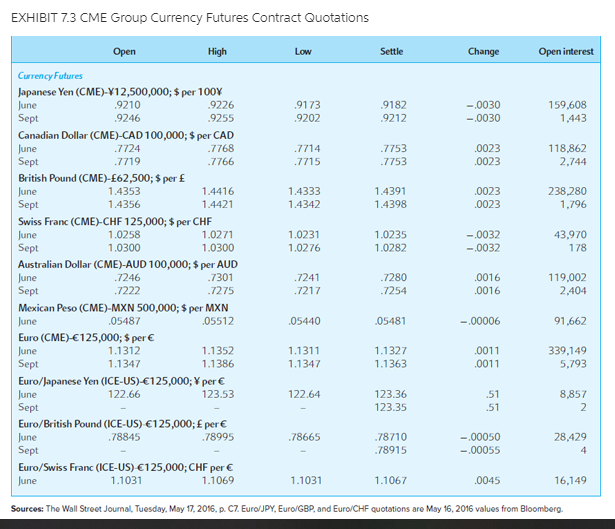

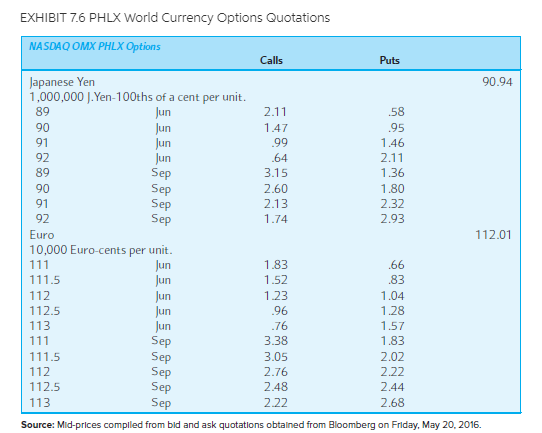

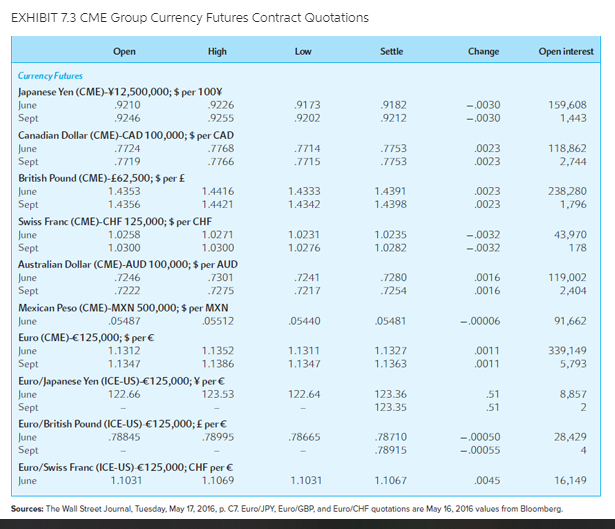

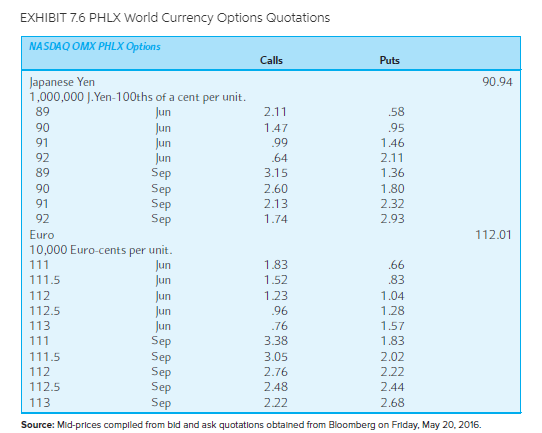

1. Cray Researdi sold a super computer to the Max Planck Institute in Germany on credit and invoiced Ell} teillieu payable in six months. Currently, the sixmoulh forward exdiauge rate is $1.1fE and the foreign exchange adviser for Cray Research predicts that the spot rate is likely to he $1.1\".l51'E in six months. (a) What is the expected gainoss from the forward hedging? {b} If you were the financial manager of Gray Research, would you recommend hedging this euro receivable? Why or why not? (c) Suppose the foreign exchange adviser predicts that the future spot rate will he the same as the forward exchange rate quoted today. Would you recommend hedging in this case? 'Why or why not? {d} Suppose now that the future spot exchange rate is forecast to be $1.1?1'5E. Would you receceruend hedging? Why or why not?I 4. Boeing just signed a contract to sell a Boeing 737 aircraft to Air France. Air France will be billed #20 million which is payable in one year. The current spot exchange rate is $1.05/{ and the one-year forward rate is $1.10/6. The annual interest rate is 6.0% in the U.S. and 5.0% in France. Boeing is concerned with the volatile exchange rate between the dollar and the euro and would like to hedge exchange exposure. (a) It is considering two hedging alternatives: sell the euro proceeds from the sale forward or borrow euros from the Credit Lyonnaise against the euro receivable. Which alternative would you recommend? Why? (b) Other things being equal, at what forward exchange rate would Boeing be indifferent between the two hedging methods?EXHIBIT 7.3 CME Group Currency Futures Contract Quotations Open High Low Settle Change Open interest Currency Futures Japanese Yen (CME)-V12,500,000; $ per 100Y June 9210 9226 9173 9187 -.0030 Sept 159.608 .9246 9255 .9202 .9212 -.0030 1.443 Canadian Dollar (CME)-CAD 100,000; $ per CAD June 7724 .7768 7714 7753 Sept .0023 .7719 118.862 .7766 .7715 .7753 .0023 2,744 British Pound (CME)-E62,500; $ per E June 1.4353 1.4416 Sept 1.4333 1.4391 0023 1.4356 1.4421 1.4342 238.280 1.4398 .0023 1,796 Swiss Franc (CME)-CHF 125,000; $ per CHF June 1.0258 1.0271 1.0231 1.0235 Sept -.0032 1.0300 1.0300 43.970 1.0276 1.0282 -.0032 178 Australian Dollar (CME)-AUD 100,000; $ per AUD June 7246 .7301 .7241 Sept .7280 0016 .7222 119,002 .7275 .7217 .7254 0016 2,404 Mexican Peso (CME)-MXN 500,000; $ per MXN June .05487 05512 05440 05481 -.00006 91.662 Euro (CME)-6125,000; $ per E June 1.1312 1.1352 1.1311 Sept 1.1347 1.1327 0011 1.1386 339.149 1.1347 1.1363 .0011 5,793 Euro/Japanese Yen (ICE-US)-(125,000; V per E June 122.66 123.53 122.64 123.36 Sept .51 8,857 123.35 .51 2 Euro/British Pound (ICE-US) (125,000; E perE June .78845 78995 78665 78710 Sept -,00050 28,429 78915 -.00055 4 Euro/Swiss Franc (ICE-US)-6125,000; CHF per E June 1.1031 1.1069 1.1031 1.1067 .0045 16,149 Sources: The Wall Street Journal, Tuesday. May 17. 2016. p. CZ. Euro/JPY. Euro/GBP, and Euro/CHF quotations are May 16, 2016 values from Bloomberg.EXHIBIT 7.6 PHLX World Currency Options Quotations NASDAQ OMX PHLX Options Calls Puts Japanese Yen 90.94 1,000,000 J. Yen-100ths of a cent per unit. 89 Jun 2.11 .58 90 Jun 1.47 .95 91 Jun .99 1.46 92 Jun 64 2.11 89 Sep 3.15 1.36 90 Sep 2.60 1.80 91 Sep 2.13 2.32 92 Sep 1.74 2.93 Euro 112.01 10,000 Euro-cents per unit. 111 Jun 1.83 .66 111.5 Jun 1.52 .83 112 Jun 1.23 1.04 112.5 Jun 96 1.28 113 Jun .76 1.57 111 Sep 3.38 1.83 111.5 Sep 3.05 2.02 112 Sep 2.76 2.22 112.5 Sep 2.48 2.44 113 Sep 2.22 2.68 Source: Mid-prices compiled from bid and ask quotations obtained from Bloomberg on Friday, May 20, 2016.Using the quotations in Exhibit 13, note that the June 201E Mexican peso futures contract has a price of 30.05431 per mm. You believe the spot price in September will be 3&06133 per MXN. What speculative position would you enter into to attempt to prot from your beliefs? Calculate your anticipated profits: assuming you take a position in three contracts. What is the size of your prot {loss} ifthe futures price is indeed an unbiased predictor of the future spot price and this price materializes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts