Question: Please show your work and formula (such as STDEV(..), AVE(..) ) how to adjust in Excel. A D E F G H 1 J K

Please show your work and formula (such as STDEV(..), AVE(..) ) how to adjust in Excel.

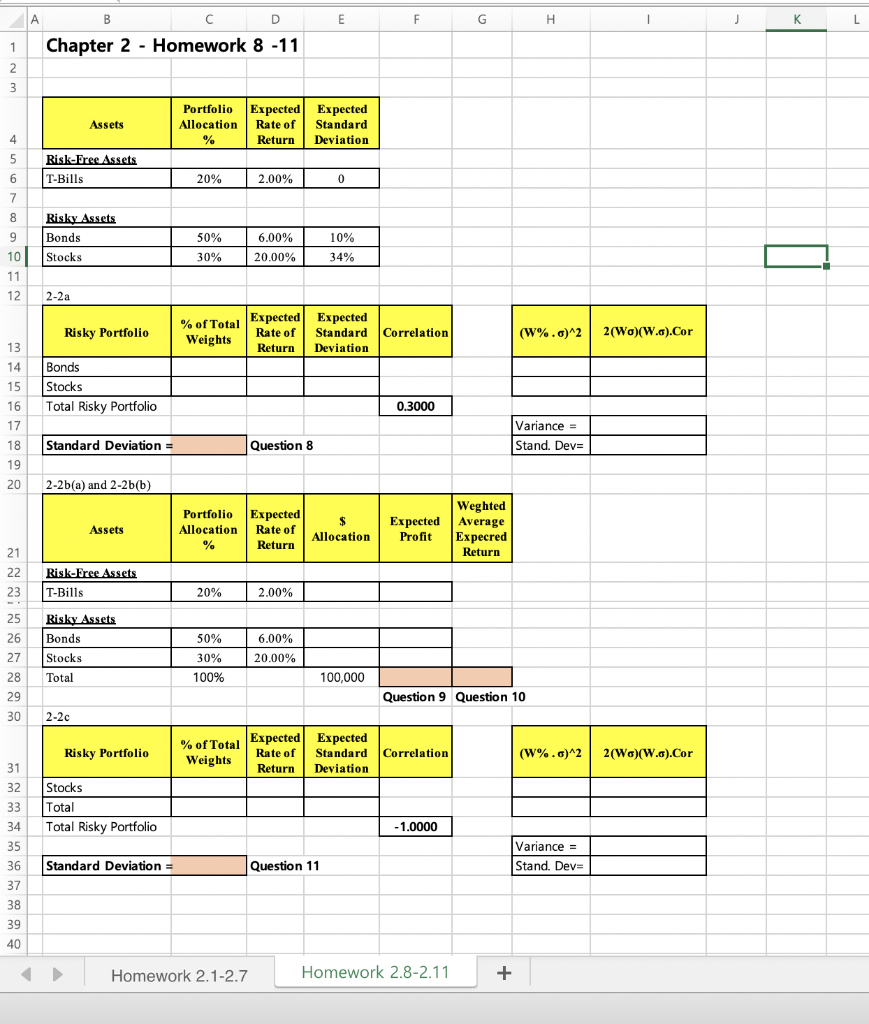

A D E F G H 1 J K L B Chapter 2 - Homework 8 -11 1 2 3 Assets Portfolio Allocation % Expected Expected Rate of Standard Return Deviation 4 5 Risk-Free Assets T-Bills 6 20% 2.00% 0 7 8 9 Risky Assets Bonds Stocks 50% 6.00% 10% 34% 10 30% 20.00% 11 12 2-2a Risky Portfolio % of Total Expected Expected Rate of Weights Standard Correlation Return Deviation (W%.c)^2 2(Wo)(W..).Cor 13 14 15 Bonds Stocks Total Risky Portfolio 16 0.3000 17 Variance = Stand. Dev= 18 Standard Deviation = Question 8 19 20 2-2b(a) and 2-2b(b) Assets Portfolio Allocation % Expected Rate of Return allocation $ Allocation Expected Profit Weghted Average Expecred Return 21 22 23 Risk-Free Assets T-Bills 20% 2.00% 25 26 27 28 Risky Assets Bonds Stocks 6.00% 50% 30% 100% 20.00% Total 100,000 29 Question 9 Question 10 30 2-2c Risky Portfolio % of Total Weights Expected Expected Rate of Standard Return Deviation Correlation (W%.6)^2 2(Wo)(W..).Cor 31 32 33 34 Stocks Total Total Risky Portfolio - 1.0000 35 Variance = Stand. Dev= 36 Standard Deviation = Question 11 37 38 39 40 Homework 2.1-2.7 Homework 2.8-2.11 + A D E F G H 1 J K L B Chapter 2 - Homework 8 -11 1 2 3 Assets Portfolio Allocation % Expected Expected Rate of Standard Return Deviation 4 5 Risk-Free Assets T-Bills 6 20% 2.00% 0 7 8 9 Risky Assets Bonds Stocks 50% 6.00% 10% 34% 10 30% 20.00% 11 12 2-2a Risky Portfolio % of Total Expected Expected Rate of Weights Standard Correlation Return Deviation (W%.c)^2 2(Wo)(W..).Cor 13 14 15 Bonds Stocks Total Risky Portfolio 16 0.3000 17 Variance = Stand. Dev= 18 Standard Deviation = Question 8 19 20 2-2b(a) and 2-2b(b) Assets Portfolio Allocation % Expected Rate of Return allocation $ Allocation Expected Profit Weghted Average Expecred Return 21 22 23 Risk-Free Assets T-Bills 20% 2.00% 25 26 27 28 Risky Assets Bonds Stocks 6.00% 50% 30% 100% 20.00% Total 100,000 29 Question 9 Question 10 30 2-2c Risky Portfolio % of Total Weights Expected Expected Rate of Standard Return Deviation Correlation (W%.6)^2 2(Wo)(W..).Cor 31 32 33 34 Stocks Total Total Risky Portfolio - 1.0000 35 Variance = Stand. Dev= 36 Standard Deviation = Question 11 37 38 39 40 Homework 2.1-2.7 Homework 2.8-2.11 +

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts