Question: Please Show your work thank you! A foreign exchange trader at Credit Suisse (Tokyo) is exploring covered interest arbitrage possibilities. He wants to invest $6,000,000

Please Show your work thank you!

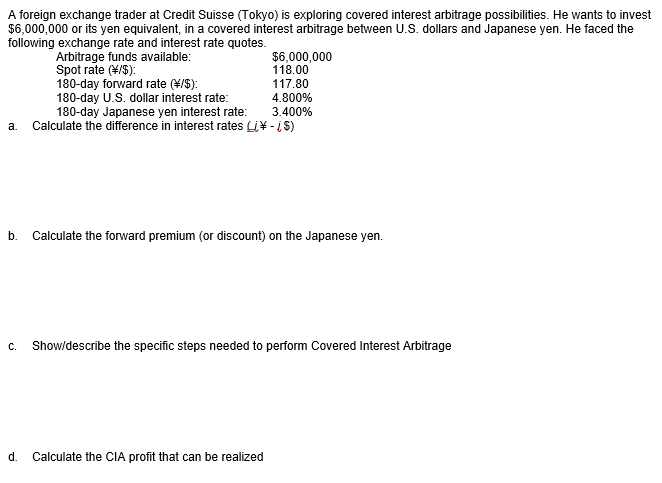

A foreign exchange trader at Credit Suisse (Tokyo) is exploring covered interest arbitrage possibilities. He wants to invest $6,000,000 or its yen equivalent, in a covered interest arbitrage between U.S. dollars and Japanese yen. He faced the following exchange rate and interest rate quotes. Arbitrage funds available: $6,000,000 Spot rate (\/$): 118.00 180-day forward rate (/%): 117.80 180-day U.S. dollar interest rate: 4.800% 180-day Japanese yen interest rate: 3.400% Calculate the difference in interest rates Li - iS) a. b. Calculate the forward premium (or discount) on the Japanese yen. C. Show/describe the specific steps needed to perform Covered Interest Arbitrage d. Calculate the CIA profit that can be realized

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts