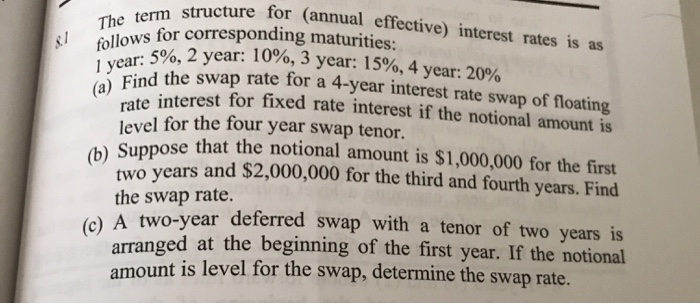

Question: please solve for (c), the answer is 0.3020 structure for (annual effective) interest rates is as The term for corresponding maturities: 8-1 follows 5%, 2

please solve for (c), the answer is 0.3020

structure for (annual effective) interest rates is as The term for corresponding maturities: 8-1 follows 5%, 2 year: 10%, 3 year: 15%, 4 year: 20% 1 ycar he swap rate for a 4-year interest rate swap of floating : 5%, Find the swap ra erest for fixed rate interest if the notional amount is level for the four year swap tenor. Suppose that the notional amount is $1,000,000 for the first ears and $2,000,000 for the third and fourth years. Find the swap rate. A two-year deferred swap with a tenor of two years is (c) arranged at the beginning of the first year. If the notional amount is level for the swap, determine the swap rate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock