Question: please solve it fast i am third time posting but not getting answer according to requirement please please i will fail if i not complete

please solve it fast i am third time posting but not getting answer according to requirement please please i will fail if i not complete this please help me

there is some parts expert completed but it is not whole question answer A to D part are done you remaining part complete it i need more then 1000 words for this . this expert part that done

please remaining part you answer me

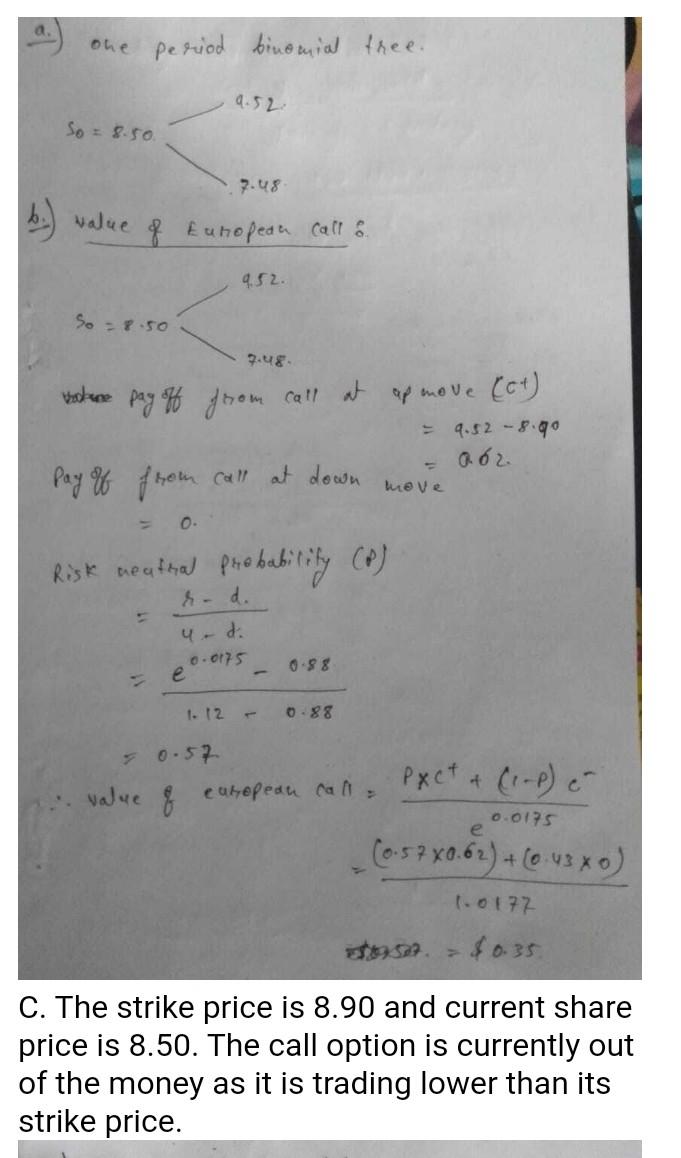

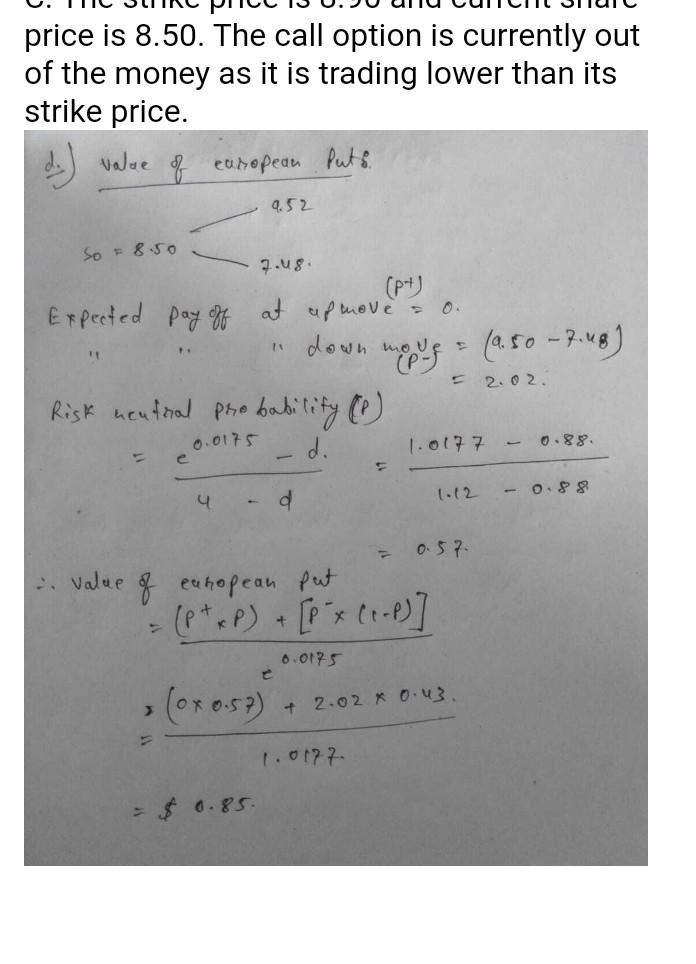

one period binemial free. 9.52 So 8.50 7.48 b.) value of European call & 4.52 so -8.50 9.48 . bokune pay off from Call at apmove (et) 4.52 -8.90 a oz. Pay off from call at down move 0. Risk neathal Probability (P) rd. 4. di 0.0175 e 0.88 1.12 0.88 0.57 Pact + (1-P) e value 8 eukepedu ca 0.0175 (0.57 80.62) + (0.430) 1.0177 09329. $ 0.35 C. The strike price is 8.90 and current share price is 8.50. The call option is currently out of the money as it is trading lower than its strike price

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts