Question: please solve part b and c only; thanks Question 12 (answer all parts) a) Suppose that two stocks, Netflix (NFLX) and Facebook (FB), have the

please solve part b and c only; thanks

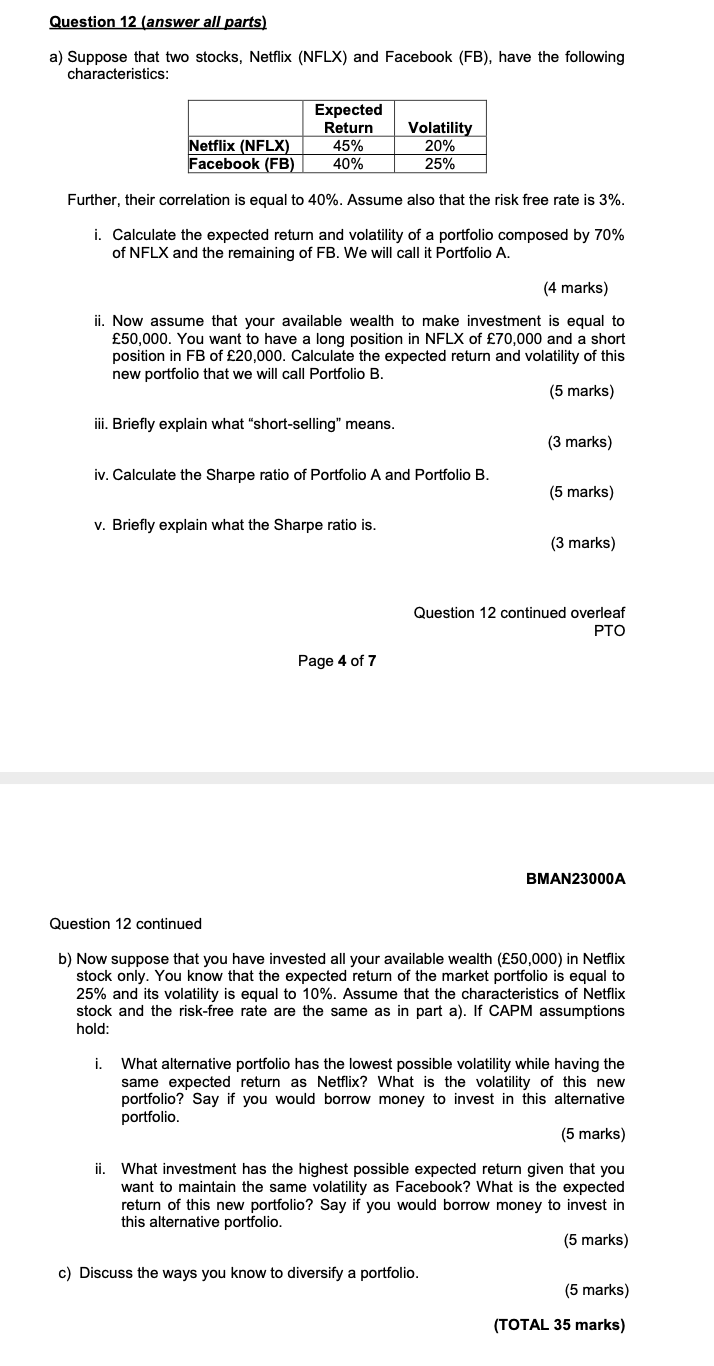

Question 12 (answer all parts) a) Suppose that two stocks, Netflix (NFLX) and Facebook (FB), have the following characteristics: Netflix (NFLX) Facebook (FB) Expected Return 45% 40% Volatility 20% 25% Further, their correlation is equal to 40%. Assume also that the risk free rate is 3%. i. Calculate the expected return and volatility of a portfolio composed by 70% of NFLX and the remaining of FB. We will call it Portfolio A. (4 marks) ii. Now assume that your available wealth to make investment is equal to 50,000. You want to have a long position in NFLX of 70,000 and a short position in FB of 20,000. Calculate the expected return and volatility of this new portfolio that we will call Portfolio B. (5 marks) iii. Briefly explain what "short-selling" means. (3 marks) iv. Calculate the Sharpe ratio of Portfolio A and Portfolio B. (5 marks) v. Briefly explain what the Sharpe ratio is. (3 marks) Question 12 continued overleaf PTO Page 4 of 7 BMAN23000A Question 12 continued b) Now suppose that you have invested all your available wealth (50,000) in Netflix stock only. You know that the expected return of the market portfolio is equal to 25% and its volatility is equal to 10%. Assume that the characteristics of Netflix stock and the risk-free rate are the same as in part a). If CAPM assumptions hold: i. What alternative portfolio has the lowest possible volatility while having the same expected return as Netflix? What is the volatility of this new portfolio? Say if you would borrow money to invest in this alternative portfolio (5 marks) ii. What investment has the highest possible expected return given that you want to maintain the same volatility as Facebook? What is the expected return of this new portfolio? Say if you would borrow money to invest in this alternative portfolio (5 marks) c) Discuss the ways you know to diversify a portfolio. (5 marks) (TOTAL 35 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts