Question: Please solve problems 1a & 1b in the Binomial Tree Model Format shown in the second picture You may work with your team to discuss

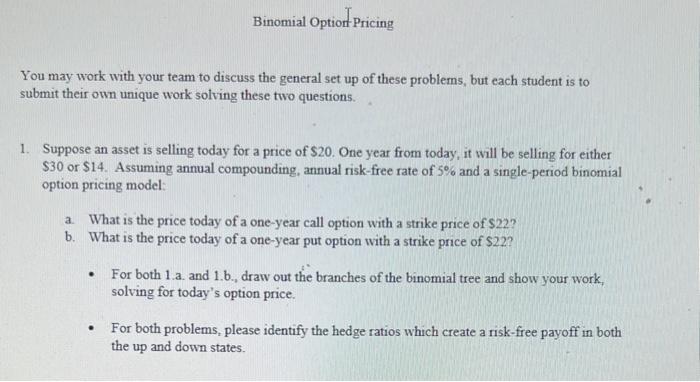

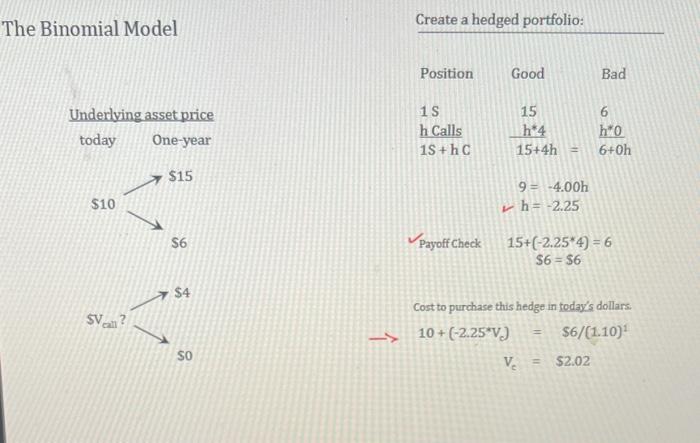

You may work with your team to discuss the general set up of these problems, but each student is to submit their own unique work solving these two questions. 1. Suppose an asset is selling today for a price of $20. One year from today, it will be selling for either $30 or $14. Assuming annual compounding, annual risk-free rate of 5% and a single-period binomial option pricing model: a. What is the price today of a one-year call option with a strike price of $22 ? b. What is the price today of a one-year put option with a strike price of $22 ? - For both 1.a. and 1.b., draw out the branches of the binomial tree and show your work, solving for today's option price. - For both problems, please identify the hedge ratios which create a risk-free payoff in both the up and down states. The Binomial Model Create a hedged portfolio: Cost to purchase this hedge in today's dollars. 10+(2.25Ve)Vc=$6/(1.10)1=$2.02

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts