Question: Please solve question 2 by showing ALL WORK using the given information to come up with the answers. (answers are included) Given the information, answer

Please solve question 2 by showing ALL WORK using the given information to come up with the answers. (answers are included)

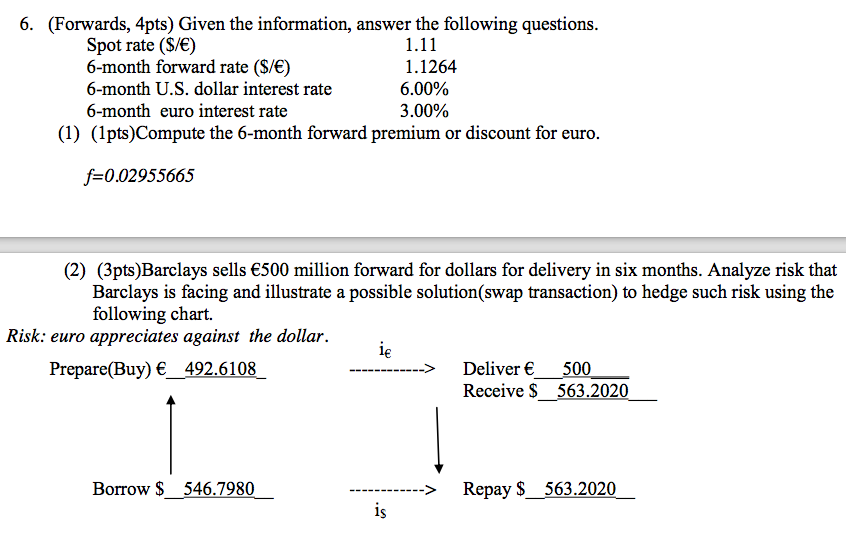

Given the information, answer the following questions. Spot rate ($/euro) 1.11 6-month forward rate ($/euro) 1.1264 6-month U.S. dollar interest rate 6.00% 6-month euro interest rate 3.00% Compute the 6-month forward premium or discount for euro. f = 0.02955665 Barclays sells euro 500 million forward for dollars for delivery in six months. Analyze risk that Barclays is facing and illustrate a possible solution(swap transaction) to hedge such risk using the following chart. Risk: euro appreciates against the dollar

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock