Question: please solve the blanks numbered 35, 36, 37, 38. please solve the blanks thank you. A stock price is currently $50. Over each of the

please solve the blanks numbered 35, 36, 37, 38.

please solve the blanks thank you.

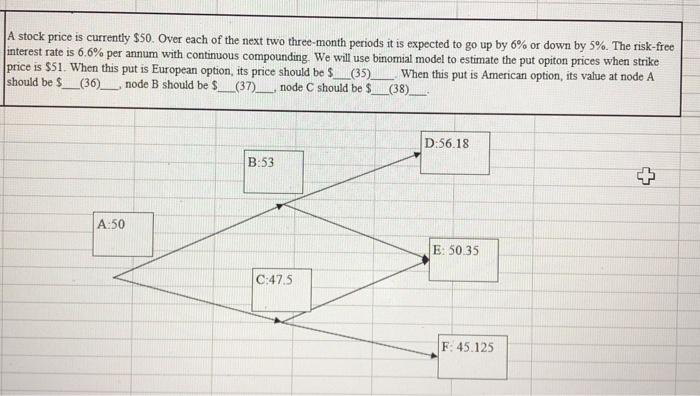

A stock price is currently $50. Over each of the next two three-month periods it is expected to go up by 6% or down by 5%. The risk-free interest rate is 6.6% per annum with continuous compounding. We will use binomial model to estimate the put opiton prices when strike price is $51. When this put is European option, its price should be $ (35) When this put is American option, its value at node A should be $__(36) _node B should be $_(37)_node C should be $_(38)__ D:56.18 B:53 + A:50 E: 50.35 C:47.5 F 45.125

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock