Question: please solve the following problem with a proof using c1,c2, and c3 throughout. Do not use a butterfly spread example. Problem 3.2 Suppose that c,

please solve the following problem with a proof using c1,c2, and c3 throughout. Do not use a butterfly spread example.

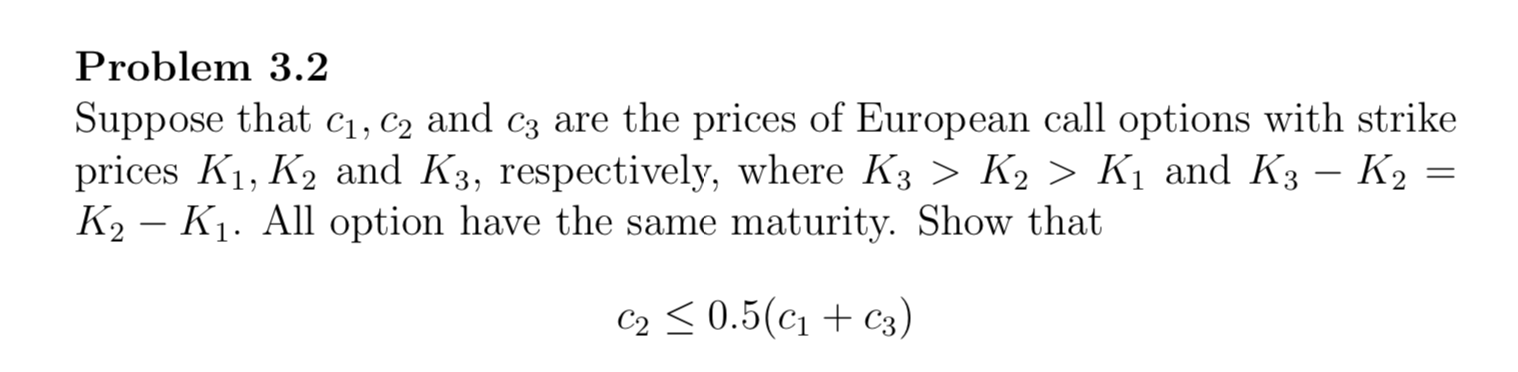

Problem 3.2 Suppose that c, C2 and c3 are the prices of European call options with strike prices K1, K2 and K3, respectively, where K3 > K2 > K1 and K3 - K2 K2-K1. All option have the same maturity. Show that C2 0.5(c1C) Problem 3.2 Suppose that c, C2 and c3 are the prices of European call options with strike prices K1, K2 and K3, respectively, where K3 > K2 > K1 and K3 - K2 K2-K1. All option have the same maturity. Show that C2 0.5(c1C)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock