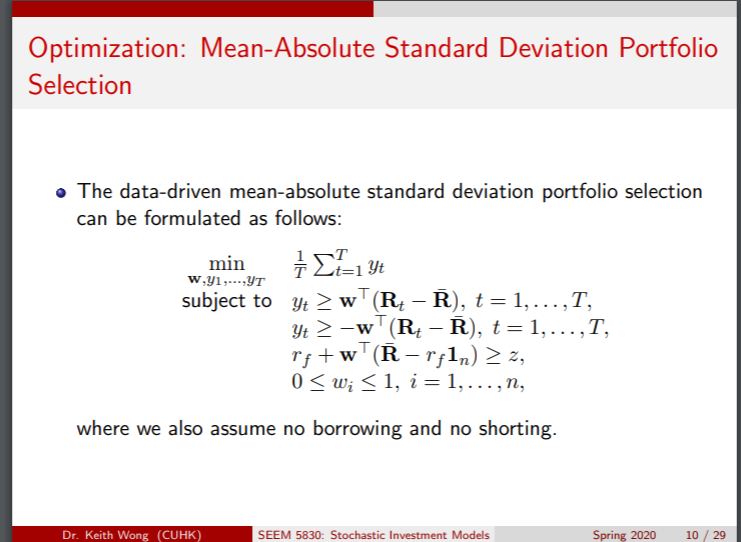

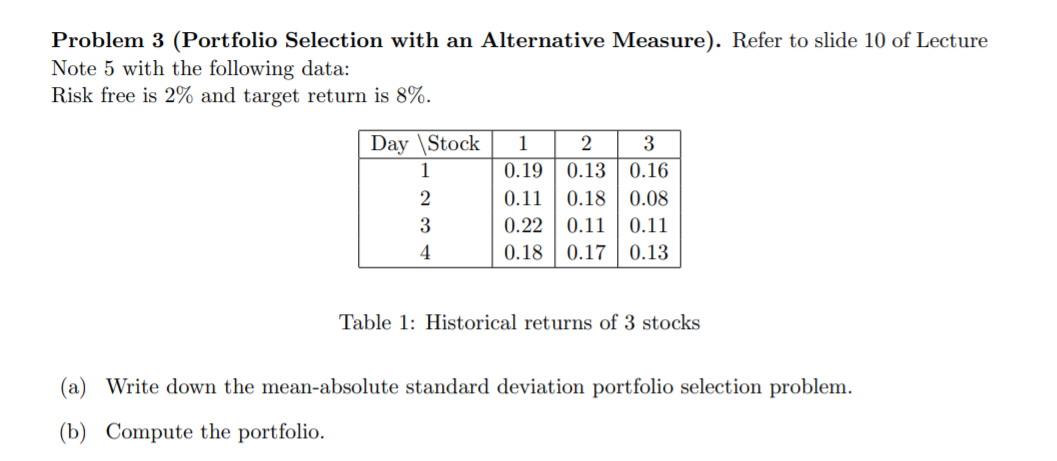

Question: please solve this question refer to the follow slide Optimization: Mean-Absolute Standard Deviation Portfolio Selection . The data-driven mean-absolute standard deviation portfolio selection can be

please solve this question refer to the follow slide

Optimization: Mean-Absolute Standard Deviation Portfolio Selection . The data-driven mean-absolute standard deviation portfolio selection can be formulated as follows: min W,yl,-...yT + Et-1 yt subject to y: > w (R - R), t= 1, ...,T, yt 2 -W (R. - R), t = 1, ...,T, rftw (R-r,ln) 2z, 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock