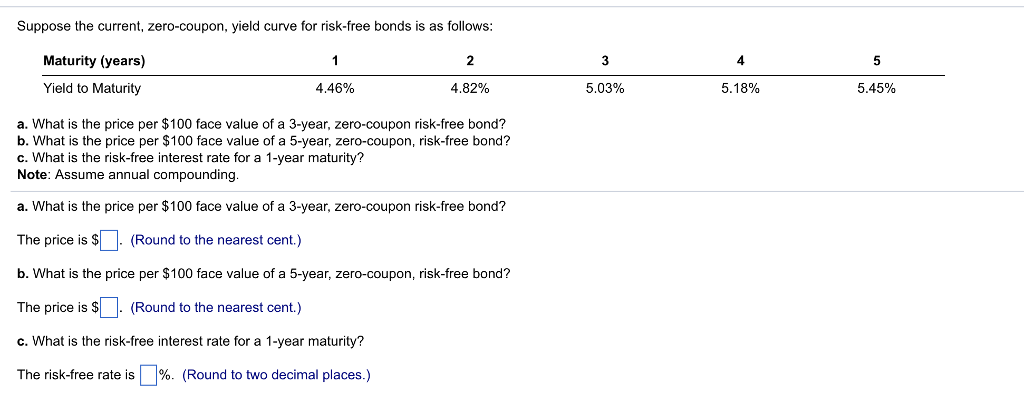

Question: Please solve this question! Suppose the current, zero-coupon, yield curve for risk-free bonds is as follows: Maturity (years) 4 Yield to Maturity 4.46% 4.82% 5.03%

Please solve this question!

Please solve this question!

Suppose the current, zero-coupon, yield curve for risk-free bonds is as follows: Maturity (years) 4 Yield to Maturity 4.46% 4.82% 5.03% 5.1 8% 5.45% a. What is the price per $100 face value of a 3-year, zero-coupon risk-free bond? b. What is the price per $100 face value of a 5-year, zero-coupon, risk-free bond? c. What is the risk-free interest rate for a 1-year maturity? Note: Assume annual compounding. a. What is the price per $100 face value of a 3-year, zero-coupon risk-free bond? The price is s- (Round to the nearest cent.) b. What is the price per $100 face value of a 5-year, zero-coupon, risk-free bond? The price is s. (Round to the nearest cent.) c. What is the risk-free interest rate for a 1-year maturity? The risk-free rate is 96. (Round to two decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts