Question: please solve using the same format in the pictures provide on excel with formulas. pictures of the excel sheet are very helpful! thanks! (Binomial Ontion

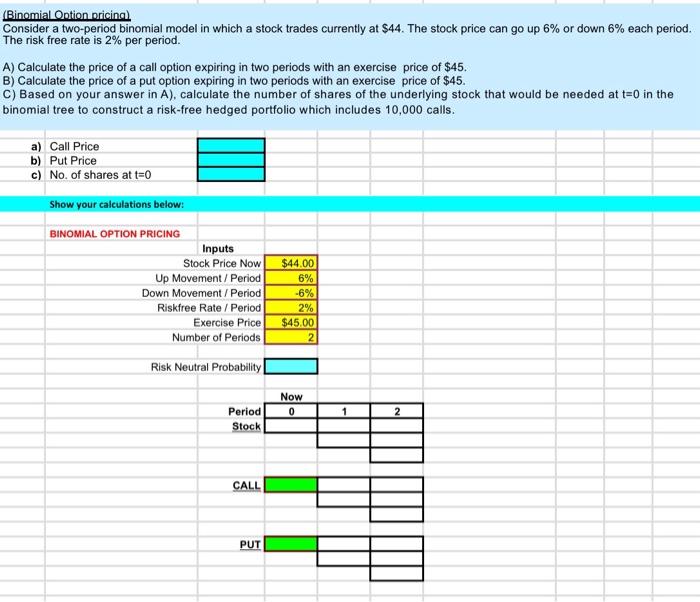

(Binomial Ontion oricina) Consider a two-period binomial model in which a stock trades currently at $44. The stock price can go up 6% or down 6% each period. The risk free rate is 2% per period. A) Calculate the price of a call option expiring in two periods with an exercise price of $45. B) Calculate the price of a put option expiring in two periods with an exercise price of $45. C) Based on your answer in A), calculate the number of shares of the underlying stock that would be needed at t=0 in the binomial tree to construct a risk-free hedged portfolio which includes 10,000 calls. a) Call Price b) Put Price c) No. of shares at t=0 Show your calculations below: BINOMIAL OPTION PRICING Inputs Stock Price Now Up Movement / Period Down Movement / Period Riskfree Rate / Period Exercise Price Number of Periods $44.00 6% 6% 2% $45.00 2 Risk Neutral Probability Now Period Stock 0 \begin{tabular}{|l|l|} \hline 1 & 2 \\ \hline & \\ \hline & \\ \hline & \\ \hline \end{tabular} CALL PUT \begin{tabular}{|l|l|} \hline & \\ \hline & \\ \hline & \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts