Question: please use clear handwriting since I am not a native speaker, and don't copy the existing answers from Course Hero and Chegg. I check them

please use clear handwriting since I am not a native speaker, and don't copy the existing answers from Course Hero and Chegg. I check them out, but hard to read them due to awful handwriting also follow the logic. Thanks!

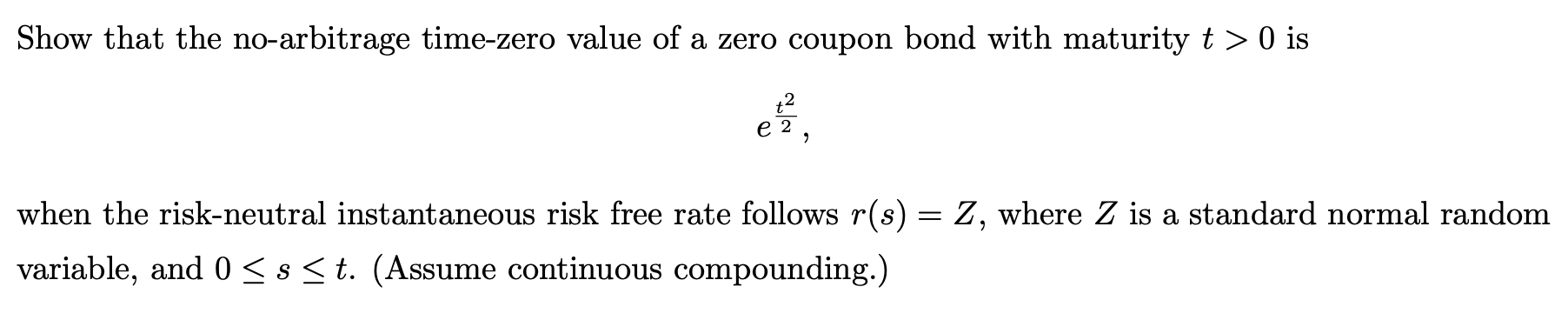

Show that the no-arbitrage time-zero value of a zero coupon bond with maturity t > 0 is e 2 , when the risk-neutral instantaneous risk free rate follows r(s) = Z, where Z is a standard normal random variable, and 0 g s S t. (Assume continuous compounding.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock