Question: Please use Excel to complete the problem below. Please submit your solution electronically. Duration and Convexity 1. What is the duration of a 12-year,

Please use Excel to complete the problem below. Please submit your solution electronically.

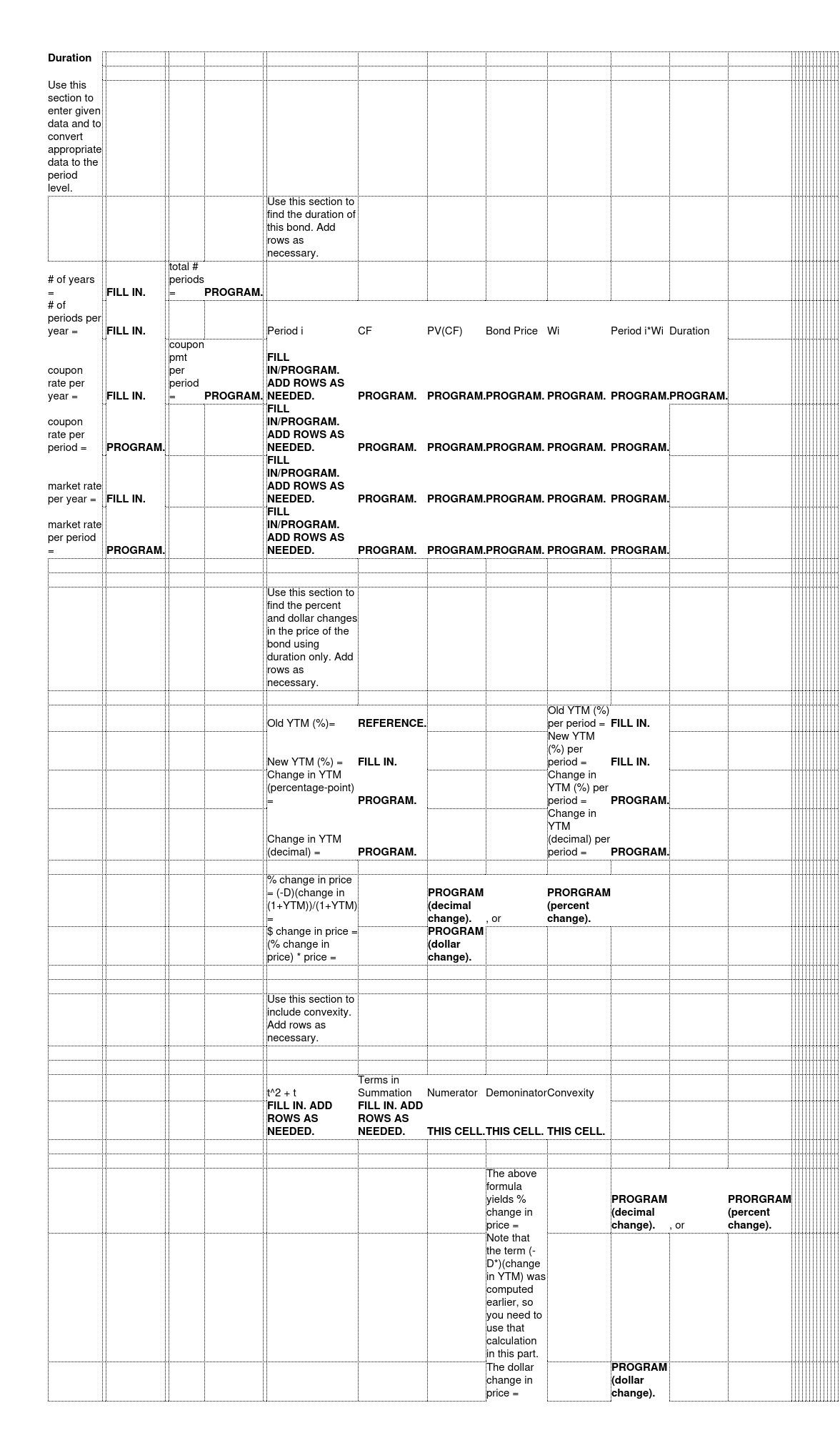

Duration and Convexity

1. What is the duration of a 12-year, 7.7% semi-annual bond if the market rate on bonds of similar quality is 7.5%?

2. Now suppose that the YTM has changed to 7.53%%. Using Macaulay duration (which is practically the same as using modified duration since you need to divide by (1+y)), what is the approximate percent change in the price of the bond? (You do not need to recalculate Macaulay duration using 7.53%. Use the duration value that you found in Problem 1.)

3. Now include convexity to estimate the percent change in the price of the bond.

Duration Use this section to enter given data and to convert appropriate data to the period level. total # # of years periods = FILL IN. = PROGRAM. # of periods per year = FILL IN. coupon pmt coupon rate per year = per period FILL IN. == Use this section to find the duration of this bond. Add rows as necessary. Period i CF PV(CF) Bond Price Wi Period i*Wi Duration FILL IN/PROGRAM. coupon rate per period = PROGRAM. market rate per year = market rate per period = FILL IN. PROGRAM. ADD ROWS AS PROGRAM. NEEDED. FILL IN/PROGRAM. ADD ROWS AS NEEDED. FILL IN/PROGRAM. ADD ROWS AS NEEDED. FILL IN/PROGRAM. ADD ROWS AS NEEDED. PROGRAM. PROGRAM.PROGRAM. PROGRAM. PROGRAM.PROGRAM. PROGRAM. PROGRAM.PROGRAM. PROGRAM. PROGRAM. PROGRAM. PROGRAM.PROGRAM. PROGRAM. PROGRAM. PROGRAM. PROGRAM.PROGRAM. PROGRAM. PROGRAM. Use this section to find the percent and dollar changes in the price of the bond using duration only. Add rows as necessary. Old YTM (%)= REFERENCE. New YTM (%) = FILL IN. Change in YTM (percentage-point) Old YTM (%) per period FILL IN. New YTM (%) per period = Change in YTM (%) per FILL IN. PROGRAM. Change in YTM (decimal) = PROGRAM. period = Change in YTM (decimal) per period = PROGRAM (decimal PRORGRAM (percent change). or change). PROGRAM % change in price = (-D)(change in (1+YTM))/(1+YTM) = $ change in price: (% change in price) * price = (dollar change). Use this section to include convexity. Add rows as necessary. t^2+t FILL IN. ADD ROWS AS NEEDED. Terms in Summation FILL IN. ADD ROWS AS NEEDED. Numerator DemoninatorConvexity THIS CELL.THIS CELL. THIS CELL. The above formula PROGRAM PROGRAM. yields % change in PROGRAM (decimal PRORGRAM (percent price = change). or change). Note that the term (- D*)(change in YTM) was computed earlier, so you need to use that calculation in this part. The dollar change in price = PROGRAM (dollar change).

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts