Question: ( Please use excell with cell refrences) An investor can design a risky portfolio based on two stocks, A and B. Stock A has an

(Please use excell with cell refrences)  An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns of A and B is .4. The risk-free rate of return is 5%.

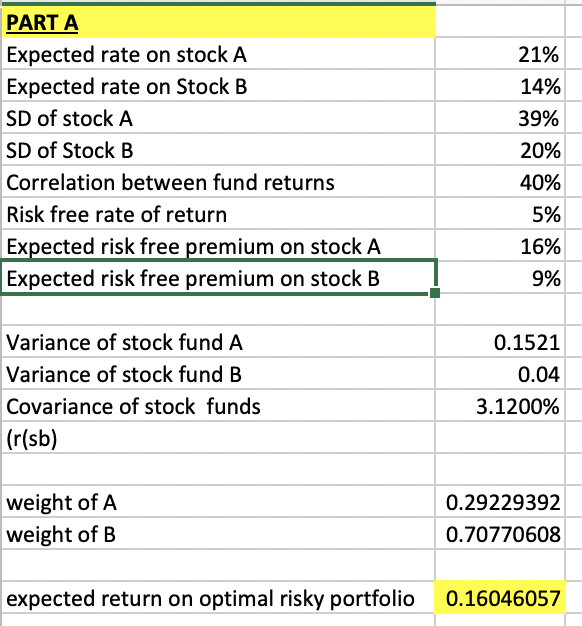

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns of A and B is .4. The risk-free rate of return is 5%.

- Find the expected return on the optimal risky portfolio. (10 point) COMPLETED ABOVE

- Suppose the investor has $1 million to invest and wants to have an expected return of 14.8% for her complete portfolio. Find the dollar amount of her investment in the risk-free asset, stock A, and Stock B. (5 points)

- Assume the returns follow a normal distribution. Calculate the probability that your portfolio value will be less than $800,000 in one year. (5 points)

PART A Expected rate on stock A Expected rate on Stock B SD of stock A SD of Stock B Correlation between fund returns Risk free rate of return Expected risk free premium on stock A Expected risk free premium on stock B 21% 14% 39% 20% 40% 5% 16% 9% Variance of stock fund A Variance of stock fund B Covariance of stock funds (r(sb) 0.1521 0.04 3.1200% weight of A weight of B 0.29229392 0.70770608 expected return on optimal risky portfolio 0.16046057 PART A Expected rate on stock A Expected rate on Stock B SD of stock A SD of Stock B Correlation between fund returns Risk free rate of return Expected risk free premium on stock A Expected risk free premium on stock B 21% 14% 39% 20% 40% 5% 16% 9% Variance of stock fund A Variance of stock fund B Covariance of stock funds (r(sb) 0.1521 0.04 3.1200% weight of A weight of B 0.29229392 0.70770608 expected return on optimal risky portfolio 0.16046057

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts