Question: PLEASE WRITE CLEARLY. THANKS! BUT thats all questions. what do you need? 2. American option Consider the following model, where r = 0, and a

PLEASE WRITE CLEARLY. THANKS!

BUT thats all questions. what do you need?

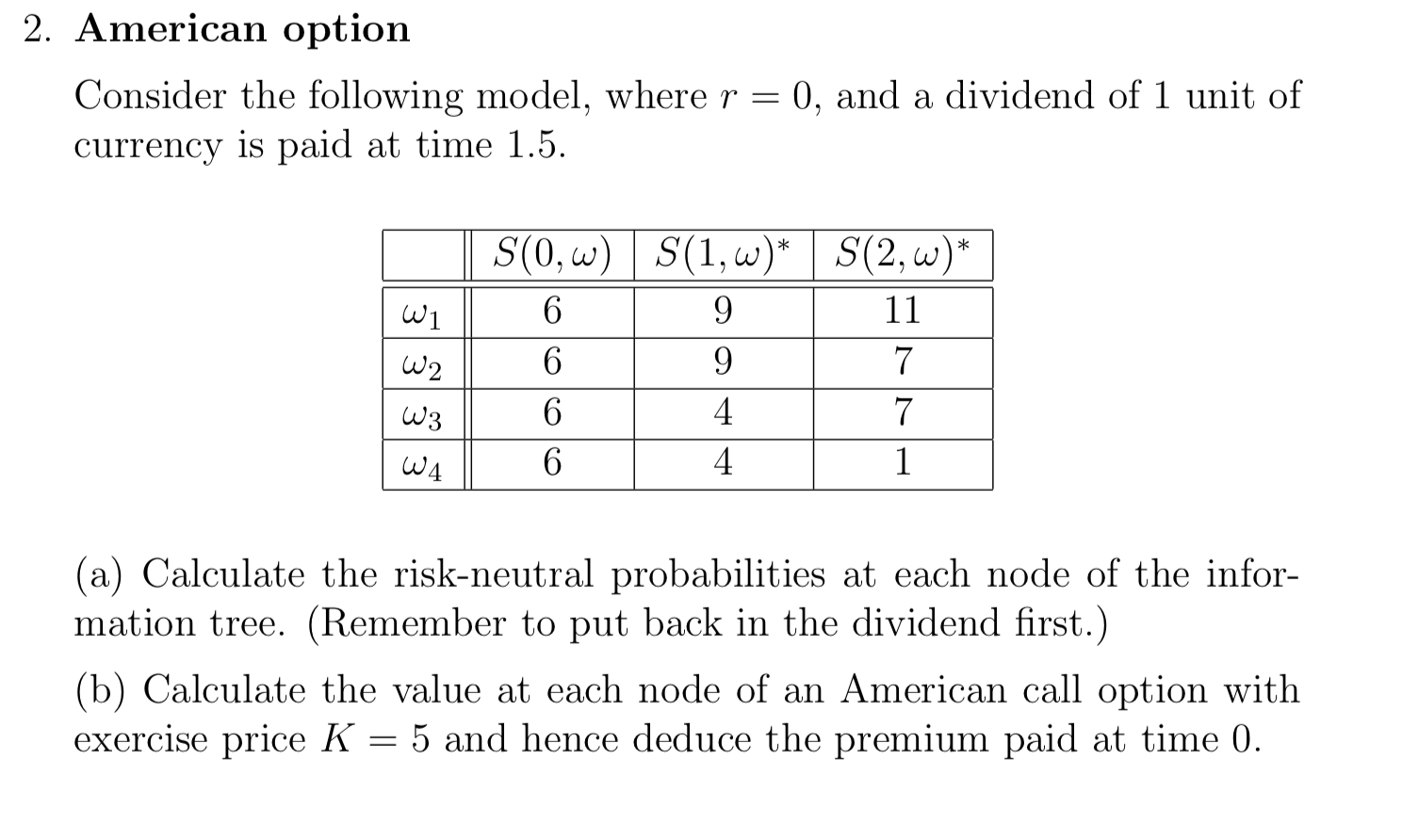

2. American option Consider the following model, where r = 0, and a dividend of 1 unit of currency is paid at time 1.5. a > * * 2 W1 W2 S(0,w) S(1,w)* S(2,w)* 6 9 11 6 9 7 6 4 7 6 4 1 W3 W4 (a) Calculate the risk-neutral probabilities at each node of the infor- mation tree. (Remember to put back in the dividend first.) (b) Calculate the value at each node of an American call option with exercise price K = 5 and hence deduce the premium paid at time 0. 2. American option Consider the following model, where r = 0, and a dividend of 1 unit of currency is paid at time 1.5. a > * * 2 W1 W2 S(0,w) S(1,w)* S(2,w)* 6 9 11 6 9 7 6 4 7 6 4 1 W3 W4 (a) Calculate the risk-neutral probabilities at each node of the infor- mation tree. (Remember to put back in the dividend first.) (b) Calculate the value at each node of an American call option with exercise price K = 5 and hence deduce the premium paid at time 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts