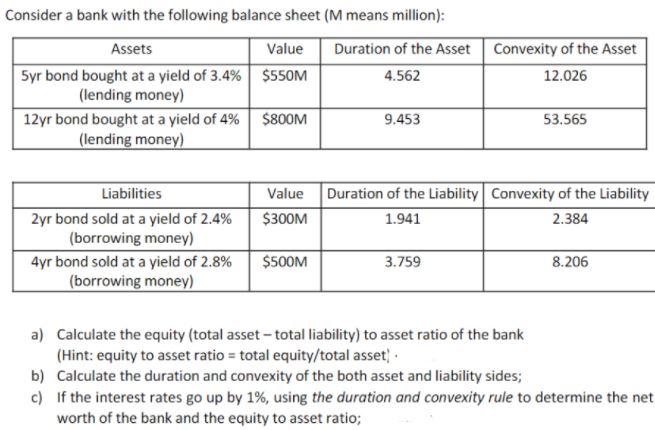

Question: pleass answer if you sure other wise skip it Consider a bank with the following balance sheet (M means million): Assets Value Duration of the

pleass answer if you sure other wise skip it

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock