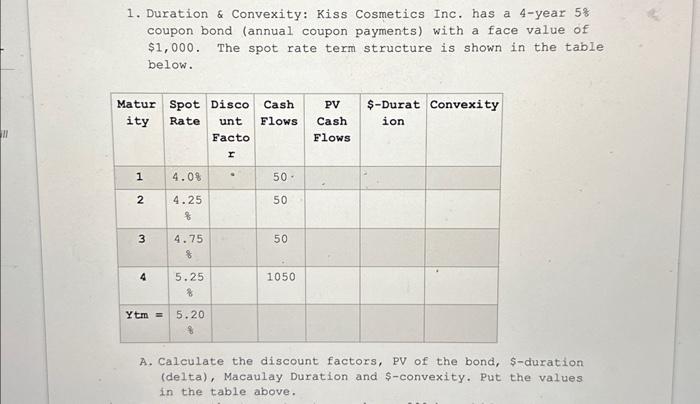

Question: plesse help answer A-E 1. Duration & Convexity: Kiss Cosmetics Inc. has a 4 -year 5% coupon bond (annual coupon payments) with a face value

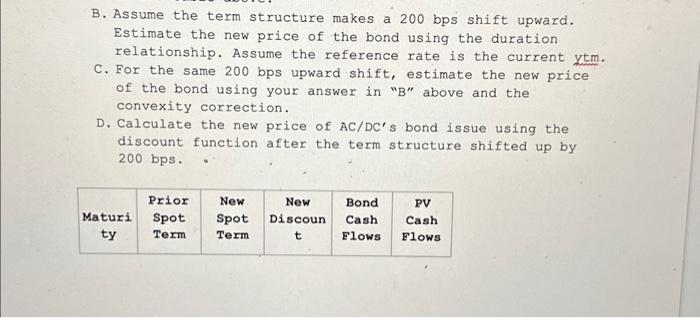

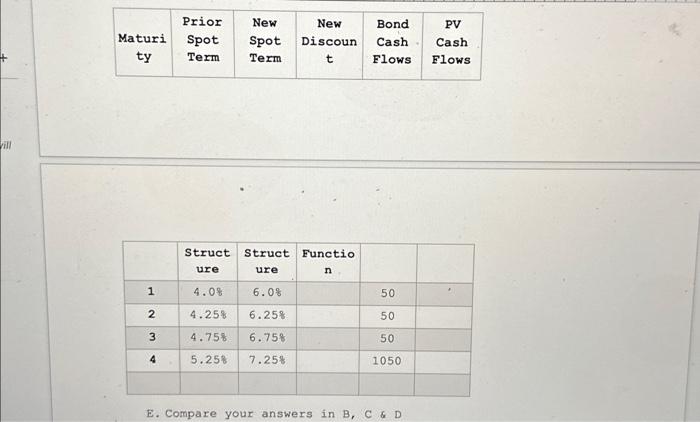

1. Duration \& Convexity: Kiss Cosmetics Inc. has a 4 -year 5% coupon bond (annual coupon payments) with a face value of $1,000. The spot rate term structure is shown in the table below. A. Calculate the discount factors, PV of the bond, \$-duration (delta), Macaulay Duration and $-convexity. Put the values in the table above. B. Assume the term structure makes a 200bps shift upward. Estimate the new price of the bond using the duration relationship. Assume the reference rate is the current ytm C. For the same 200 bps upward shift, estimate the new price of the bond using your answer in " B " above and the convexity correction. D. Calculate the new price of AC/DC 's bond issue using the discount function after the term structure shifted up by 200 bps. . E. Compare your answers in B, C \& D

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts