Question: plz answer this question Suppose that the current level of the S&P 500 is as shown below. The annualized dividend yield on the S&P 500,

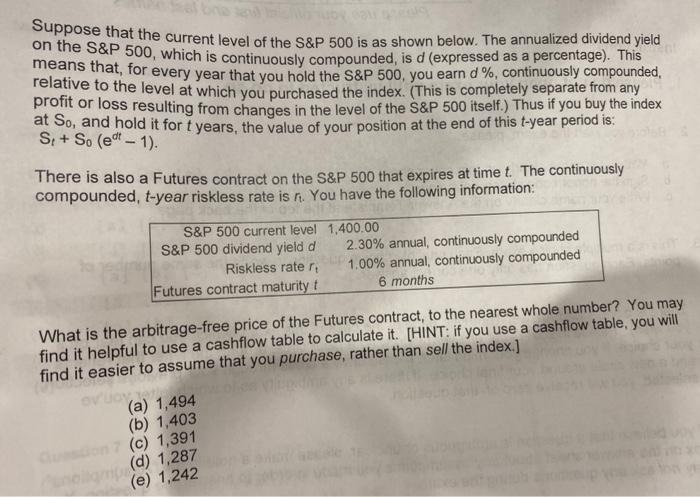

Suppose that the current level of the S&P 500 is as shown below. The annualized dividend yield on the S&P 500, which is continuously compounded, is d (expressed as a percentage). This means that, for every year that you hold the S&P 500, you earn d %, continuously compounded, relative to the level at which you purchased the index. This is completely separate from any profit or loss resulting from changes in the level of the S&P 500 itself.) Thus if you buy the index at So, and hold it for t years, the value of your position at the end of this t-year period is: S; + So (ed' - 1). There is also a Futures contract on the S&P 500 that expires at time t. The continuously compounded, t-year riskless rate is n. You have the following information: - S&P 500 current level 1,400.00 S&P 500 dividend yield d 2.30% annual, continuously compounded Riskless rater 1.00% annual, continuously compounded Futures contract maturity t 6 months What is the arbitrage-free price of the Futures contract, to the nearest whole number? You may find it helpful to use a cashflow table to calculate it [HINT: if you use a cashflow table, you will find it easier to assume that you purchase, rather than sell the index.] (a) 1,494 (b) 1,403 (c) 1,391 (d) 1,287 (e) 1,242

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts