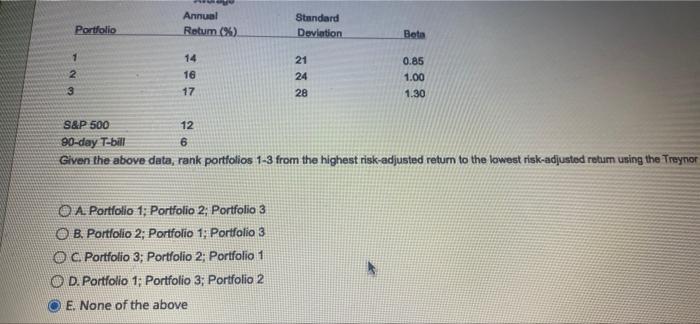

Question: Portfolio Annual Retum (%) Standard Deviation Beta 1 2 3 14 16 17 21 24 28 0.85 1.00 1.30 S&P 500 12 90-day T-bill 6

Portfolio Annual Retum (%) Standard Deviation Beta 1 2 3 14 16 17 21 24 28 0.85 1.00 1.30 S&P 500 12 90-day T-bill 6 Given the above data, rank portfolios 1-3 from the highest risk-adjusted return to the lowest risk-adjusted retum using the Treynor O A Portfolio 1; Portfolio 2 Portfolio 3 OB Portfolio 2; Portfolio 1; Portfolio 3 OC Portfolio 3; Portfolio 2; Portfolio 1 OD. Portfolio 1; Portfolio 3; Portfolio 2 O E None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock