On a weekend in late October 2015, Albert sat over his breakfast, and imitated of his...

Fantastic news! We've Found the answer you've been seeking!

Question:

![Background Material (Pick the right equation based on your need) Mean = E(R) E(R) = S(r) R, = wR1 + R2 + ... + w,R E[R] = Wil](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2021/02/602cf6e4db268_1613559522769.jpg)

Transcribed Image Text:

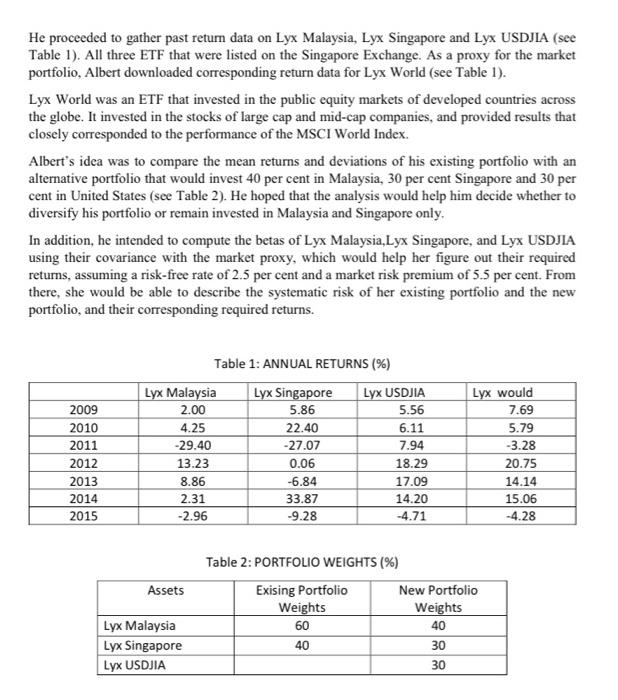

On a weekend in late October 2015, Albert sat over his breakfast, and imitated of his personal investment portfolio over the past seven years. He remembered that, after the financial crisis in 2007-08, he had been advised to avoid U.S. stocks and to put his savings in the emerging economies of Malaysia and Singapore. Therefore, he decided to distribute his funds to two exchange traded funds (ETF) invested in the equity markets of Malaysia and Singapore, namely Lyx Malaysia and Lyx Singapore, in the ratio of 60 per cent and 40 per cent respectively. Although Albert had been satisfied with his portfolio performance over the past seven years. The high growth in these two emerging markets had failed out lately. However the advice he had gathered from analysts' reports implied that he should stay invested in these markets, notwithstanding with more attention to the volatile strikes. PORTFOLIO DIVERSIFICATION Albert had enrolled in a corporate finance class on risk and return to improve his investment knowledge. During the classes, he Leamed that the risk of portfolio was not simply a weighted average of the individual variances of the component assets. Rather, it was determined to a large extent by the co-movement between the returns of the component assets. Accordingly, Albert reasoned that diversification to include an asset that was imperfectly correlated with the existing components of his portfolio should decrease his risk without sacrificing returns, if he had understood correctly. With this understanding, Albert tried to search for an asset that was not correlated with Lyx Malaysia or Lyx Singapore. THE RECOVERING U.S. EQUITY MARKET Albert wondered whether he should move some of her funds to U.S. equity. The U.S. economy appeared to have benefitted from the rounds of quantitative casing and was finally recovering from the doldrums. The U.S. unemployment data had improved and there was speculation that the Federal Reserve might raise interest. Surely, the fact that the United Stated was picking up at a time when Malaysia and Singapore were slowing down was indicative of low correlation among the three economies. FINANCILA ANALYSIS To confirm his idea, Albert decided to pick an ETF that tracked the U.S. equity market. He observed that Lyx United States Dow Jones Industrial Average (USDJA) was invested in the public equity markets of the United States, in the stocks of companies operating across diversified sectors, excluding transportation and utilities sectors. He proceeded to gather past return data on Lyx Malaysia, Lyx Singapore and Lyx USDJIA (see Table 1). All three ETF that were listed on the Singapore Exchange. As a proxy for the market portfolio, Albert downloaded corresponding return data for Lyx World (see Table 1). Lyx World was an ETF that invested in the public equity markets of developed countries across the globe. It invested in the stocks of large cap and mid-cap companies, and provided results that closely corresponded to the performance of the MSCI World Index. Albert's idea was to compare the mean returns and deviations of his existing portfolio with an alternative portfolio that would invest 40 per cent in Malaysia, 30 per cent Singapore and 30 per cent in United States (see Table 2). He hoped that the analysis would help him decide whether to diversify his portfolio or remain invested in Malaysia and Singapore only. In addition, he intended to compute the betas of Lyx Malaysia, Lyx Singapore, and Lyx USDJIA using their covariance with the market proxy, which would help her figure out their required returns, assuming a risk-free rate of 2.5 per cent and a market risk premium of 5.5 per cent. From there, she would be able to describe the systematic risk of her existing portfolio and the new portfolio, and their corresponding required returns. 2009 2010 2011 2012 2013 2014 2015 Lyx Malaysia 2.00 4.25 -29.40 13.23 8.86 2.31 -2.96 Assets Table 1: ANNUAL RETURNS (%) Lyx Malaysia Lyx Singapore Lyx USDJIA Lyx Singapore Lyx USDJIA 5.86 5.56 22.40 6.11 -27.07 7.94 18.29 0.06 -6.84 33.87 -9.28 17.09 14.20 -4.71 Table 2: PORTFOLIO WEIGHTS (%) Exising Portfolio Weights 60 40 Lyx would 7.69 5.79 -3.28 20.75 New Portfolio Weights 40 30 30 14.14 15.06 -4.28 Questions: 1- Using the given information in Table 1, calculate the mean return, standard deviation, covariance and correlation for the given stocks. (Time allocated: 15 minutes) 2- Calculate the return and standard deviation for the portfolio consisting of the two stocks. (Time allocated: 15 minutes) 3- After adding the stock Lyx USDJIA, what is the portfolio return and standard deviation? How does the new portfolio differ from the first portfolio calculate in question 2? (Time allocated: 15 minutes) 4- Based on your analysis, explain should Albert diversify his portfolio or remain invested in Malaysia and Singapore only? (Time allocated: 15 minutes) 5- Calculate beta for the current portfolio and the new portfolio. Assuming a risk free rate of 2.5% and a market risk premium of 5.5% and calculate the expected return for both portfolios. (Time allocated: 15 minutes) Background Material (Pick the right equation based on your need) Mean = E[R] E(R) = {Σ(r.) R₁ = w₁R₁ + w₂R₂ + E[R₂] = 0= *Pab= = wifi+w₂/2 + ...Wnfln Σ(r.-E(r.)) n-1 Var Rp] = wo+wot+2wawsCOV [Ra, Rs] = wo + wio? + 2wawsoa@bPab COV R.R dags +wnRn COV Ra, Rb] = Pabab E[R₂] = Rpremium = E[Rm] - T₁ E[R]=r; +3₁ x (E[Rm]-rs) Cov(R₁, Rm) B₁ = Var(Rm) = wifi + *** +wntn On a weekend in late October 2015, Albert sat over his breakfast, and imitated of his personal investment portfolio over the past seven years. He remembered that, after the financial crisis in 2007-08, he had been advised to avoid U.S. stocks and to put his savings in the emerging economies of Malaysia and Singapore. Therefore, he decided to distribute his funds to two exchange traded funds (ETF) invested in the equity markets of Malaysia and Singapore, namely Lyx Malaysia and Lyx Singapore, in the ratio of 60 per cent and 40 per cent respectively. Although Albert had been satisfied with his portfolio performance over the past seven years. The high growth in these two emerging markets had failed out lately. However the advice he had gathered from analysts' reports implied that he should stay invested in these markets, notwithstanding with more attention to the volatile strikes. PORTFOLIO DIVERSIFICATION Albert had enrolled in a corporate finance class on risk and return to improve his investment knowledge. During the classes, he Leamed that the risk of portfolio was not simply a weighted average of the individual variances of the component assets. Rather, it was determined to a large extent by the co-movement between the returns of the component assets. Accordingly, Albert reasoned that diversification to include an asset that was imperfectly correlated with the existing components of his portfolio should decrease his risk without sacrificing returns, if he had understood correctly. With this understanding, Albert tried to search for an asset that was not correlated with Lyx Malaysia or Lyx Singapore. THE RECOVERING U.S. EQUITY MARKET Albert wondered whether he should move some of her funds to U.S. equity. The U.S. economy appeared to have benefitted from the rounds of quantitative casing and was finally recovering from the doldrums. The U.S. unemployment data had improved and there was speculation that the Federal Reserve might raise interest. Surely, the fact that the United Stated was picking up at a time when Malaysia and Singapore were slowing down was indicative of low correlation among the three economies. FINANCILA ANALYSIS To confirm his idea, Albert decided to pick an ETF that tracked the U.S. equity market. He observed that Lyx United States Dow Jones Industrial Average (USDJA) was invested in the public equity markets of the United States, in the stocks of companies operating across diversified sectors, excluding transportation and utilities sectors. He proceeded to gather past return data on Lyx Malaysia, Lyx Singapore and Lyx USDJIA (see Table 1). All three ETF that were listed on the Singapore Exchange. As a proxy for the market portfolio, Albert downloaded corresponding return data for Lyx World (see Table 1). Lyx World was an ETF that invested in the public equity markets of developed countries across the globe. It invested in the stocks of large cap and mid-cap companies, and provided results that closely corresponded to the performance of the MSCI World Index. Albert's idea was to compare the mean returns and deviations of his existing portfolio with an alternative portfolio that would invest 40 per cent in Malaysia, 30 per cent Singapore and 30 per cent in United States (see Table 2). He hoped that the analysis would help him decide whether to diversify his portfolio or remain invested in Malaysia and Singapore only. In addition, he intended to compute the betas of Lyx Malaysia, Lyx Singapore, and Lyx USDJIA using their covariance with the market proxy, which would help her figure out their required returns, assuming a risk-free rate of 2.5 per cent and a market risk premium of 5.5 per cent. From there, she would be able to describe the systematic risk of her existing portfolio and the new portfolio, and their corresponding required returns. 2009 2010 2011 2012 2013 2014 2015 Lyx Malaysia 2.00 4.25 -29.40 13.23 8.86 2.31 -2.96 Assets Table 1: ANNUAL RETURNS (%) Lyx Malaysia Lyx Singapore Lyx USDJIA Lyx Singapore Lyx USDJIA 5.86 5.56 22.40 6.11 -27.07 7.94 18.29 0.06 -6.84 33.87 -9.28 17.09 14.20 -4.71 Table 2: PORTFOLIO WEIGHTS (%) Exising Portfolio Weights 60 40 Lyx would 7.69 5.79 -3.28 20.75 New Portfolio Weights 40 30 30 14.14 15.06 -4.28 Questions: 1- Using the given information in Table 1, calculate the mean return, standard deviation, covariance and correlation for the given stocks. (Time allocated: 15 minutes) 2- Calculate the return and standard deviation for the portfolio consisting of the two stocks. (Time allocated: 15 minutes) 3- After adding the stock Lyx USDJIA, what is the portfolio return and standard deviation? How does the new portfolio differ from the first portfolio calculate in question 2? (Time allocated: 15 minutes) 4- Based on your analysis, explain should Albert diversify his portfolio or remain invested in Malaysia and Singapore only? (Time allocated: 15 minutes) 5- Calculate beta for the current portfolio and the new portfolio. Assuming a risk free rate of 2.5% and a market risk premium of 5.5% and calculate the expected return for both portfolios. (Time allocated: 15 minutes) Background Material (Pick the right equation based on your need) Mean = E[R] E(R) = {Σ(r.) R₁ = w₁R₁ + w₂R₂ + E[R₂] = 0= *Pab= = wifi+w₂/2 + ...Wnfln Σ(r.-E(r.)) n-1 Var Rp] = wo+wot+2wawsCOV [Ra, Rs] = wo + wio? + 2wawsoa@bPab COV R.R dags +wnRn COV Ra, Rb] = Pabab E[R₂] = Rpremium = E[Rm] - T₁ E[R]=r; +3₁ x (E[Rm]-rs) Cov(R₁, Rm) B₁ = Var(Rm) = wifi + *** +wntn

Expert Answer:

Answer rating: 100% (QA)

Answer 1 The Means SD Variance covariance and correlation are shown below The ... View the full answer

Related Book For

Accounting Volume 2

ISBN: 978-0176509743

2nd Canadian edition

Authors: James Reeve, Jonathan Duchac, Sheila Elworthy, Carl S. Warren

Posted Date:

Students also viewed these mathematics questions

-

Calculate the amount of accumulations bevond current needs for XYZ corporation.

-

Solomon Books buys books and magazines directly from publishers and distributes them to grocery stores. The wholesaler expects to purchase the following inventory: April May June Required purchases...

-

A large sheet has charge density 0,= +764 x10-12 C/m A cylindrical Gaussian surface (dashed lines) encloses a portion of the sheet and extends a distance Lo on either side of the sheet. The areas of...

-

Let f: RR be a differentiable function such that its derivative f' is continuous and f(n) = 6. If F: [0, 1 by F(x) = f(t)dt, , and if ] R is defined (f'(x)+F(x)) cosx dx = 2 0 then the value of f(0)...

-

Department A uses 5,000 square feet of floor space, department B uses 2,500, department C uses 4,300, and department D uses 2,700. The total overhead is $8,200. Find each department's overhead based...

-

In some circumstances the contribution of one neutrino flavor can be approximately neglected; e.g., in \(u_{\mu} ightarrow u_{\tau}\) atmospheric oscillations the role played by the \(u_{e}\) is very...

-

The mean room and board expense per year at four-year colleges is \($10,453\). You randomly select 9 four-year colleges. What is the probability that the mean room and board is less than \($10,750?\)...

-

PWC Systems Inc. makes personal watercraft for sale through specialty sporting goods stores. The company has a standard model but also makes custom-designed models. Management has designed an ABC...

-

Forensic psychology is an attempt to reinvent itself and lacks originality. Discuss the value of forensic psychology to the criminal justice system.?

-

Nike, Inc. , had the following condensed balance sheet on May 31, 2011 ($ in millions): Suppose the following transactions occurred during the first 3 days of June ($ in millions): 1. Nike acquired...

-

explains the significance of the following key concepts in corporate strategic management: VUCA environment, Corporate Foresight, Resource Based View of the Firm, Dynamic Capabilities Framework,...

-

1. 2. 3. Suppose that the long-run world demand and supply elasticities of crude oil are -0.906 and 0.515, respectively. The current long-run equilibrium price is $30 per barrel and the equilibrium...

-

ANSWER THE FOLLOWING QUESTION AND PROVIDE SOLUTIONS : Problem 9.1 COMPREHENSIVE Valkyrie reported the following income during the year. Service Fees Interest Income from bank deposits Royalties from...

-

A non-dividend-paying stock has a current price of 800 ngwee. In any unit of time (t, t + 1) the price of the stock either increases by 25% or decreases by 20%. K1 held in cash between times t and t...

-

New Heritage Doll Company Executive Summary: (Explain what the situation is and what is at stake) Assumptions: Please list assumptions you make for each case and explain the rationale behind your...

-

What is the range? Restrict the domain of f(x) = (x-6) + 12 so that it is a one-to-one function. What will the domain be? Determine the inverse function, f-1(x).

-

One product line of Anita's Accessories (AA) is the assembly, testing, and marketing of a USB thumb drive - The Speedster. The parts list for each unit is: 1 standard USB plug, 1 USB mass storage...

-

If a and b are positive numbers, find the maximum value of f ( x ) = x a (9 x ) b on the interval 0 x 9.

-

Cassidy Ltd. purchased $80,000 Stump Inc., 3% bonds at par value on October 1, 2015. Cassidy intends to hold the bonds to maturity in 2025. The bonds pay interest on October 1 and April 1. On April...

-

Brighttime Business Centre Ltd. reported the following accounts and their balances as at January 1, 2015, the beginning of the current fiscal year: The company reported the following results for the...

-

1. Michael and Matthew will each pay their share of income tax on the business income when they file their personal income tax returns. 2. Sharon is responsible for all the debts of the business. 3....

-

Transactions for Thorn Consulting for the month of June are presented below. Identify the accounts to be debited and credited for each transaction. June 1 2 Oleg Thorn invests 5,000 cash in a small...

-

Emily Stansbury is a licensed dentist. During the first month of the operation of her business, the following events and transactions occurred. Emily uses the following chart of accounts: No. 101...

-

Indicate how a journal is used in the recording process.

Study smarter with the SolutionInn App