Question: Portfolio theory question. Please help me solve this ASAP! It's okay if you can't solve every question, please help me as much as you can.

Portfolio theory question. Please help me solve this ASAP! It's okay if you can't solve every question, please help me as much as you can. It will really help my learning . I appreciate it thanks.

. I appreciate it thanks.

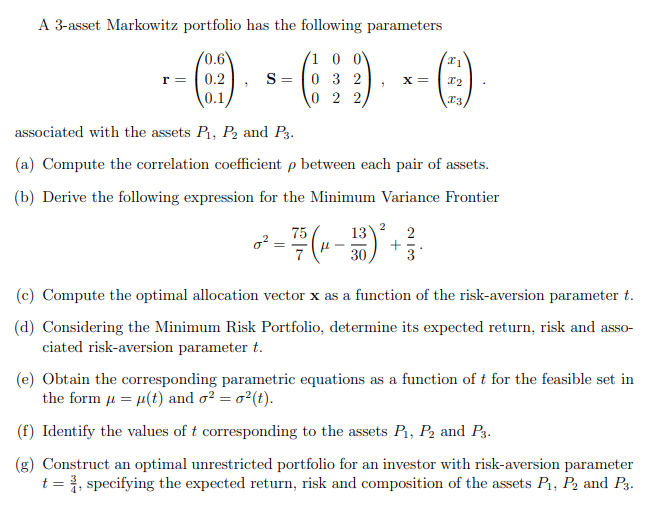

A 3-asset Markowitz portfolio has the following parameters 21 r= (0.6 0.2 0.1 (1 0 0 S= 0 3 2 0 2 2 22 13 associated with the assets P1, P, and Pz. (a) Compute the correlation coefficient p between each pair of assets. (b) Derive the following expression for the Minimum Variance Frontier 02=(-- 33) 13 30 2 2 + (c) Compute the optimal allocation vector x as a function of the risk-aversion parameter t. (d) Considering the Minimum Risk Portfolio, determine its expected return, risk and asso- ciated risk-aversion parameter t. (e) Obtain the corresponding parametric equations as a function of t for the feasible set in the form p= u(t) and o2 = 0%(t). (f) Identify the values of t corresponding to the assets P1, P, and P3. (g) Construct an optimal unrestricted portfolio for an investor with risk-aversion parameter t = x, specifying the expected return, risk and composition of the assets P1, P, and P3. A 3-asset Markowitz portfolio has the following parameters 21 r= (0.6 0.2 0.1 (1 0 0 S= 0 3 2 0 2 2 22 13 associated with the assets P1, P, and Pz. (a) Compute the correlation coefficient p between each pair of assets. (b) Derive the following expression for the Minimum Variance Frontier 02=(-- 33) 13 30 2 2 + (c) Compute the optimal allocation vector x as a function of the risk-aversion parameter t. (d) Considering the Minimum Risk Portfolio, determine its expected return, risk and asso- ciated risk-aversion parameter t. (e) Obtain the corresponding parametric equations as a function of t for the feasible set in the form p= u(t) and o2 = 0%(t). (f) Identify the values of t corresponding to the assets P1, P, and P3. (g) Construct an optimal unrestricted portfolio for an investor with risk-aversion parameter t = x, specifying the expected return, risk and composition of the assets P1, P, and P3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts