Question: #Precisy the formulas you will use (DO NOT USE EXCEL) Problem 3 (10 points) Looking ahead to next year, the expected returns for ABC Company

#Precisy the formulas you will use (DO NOT USE EXCEL)

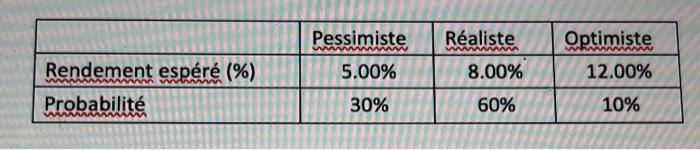

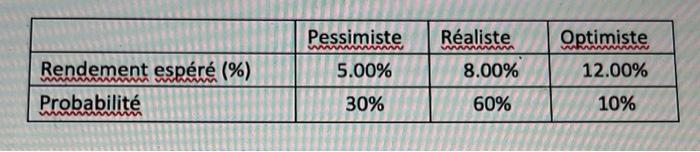

Problem 3 (10 points) Looking ahead to next year, the expected returns for ABC Company stock, given different predictions and their respective probabilities, would be summarized in the following table:

a) Calculate the expected return of firm ABC. (2 points) b) Calculate the standard deviation of returns for firm ABC. (2 points) You have a sum of money that you plan to invest in the stock market.

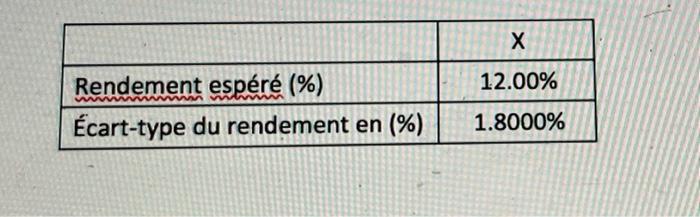

c) If you wanted to invest in only one of these two securities, X or Y, which would you consider? Why? (2 points) d) If you decide to invest 60% of your assets in stock X and 40% in stock Y, calculate the expected return and the standard deviation of your portfolio knowing that the correlation coefficient between the two titles is 0.73. (2 points) e) If you decide to invest 45% of your assets in stock X and the rest in a bond risk-free Canadian government offering an annual return of 6%, calculate the expected return and the standard deviation of the returns of your new portfolio. (2 points)

Raliste WAWA w Pessimiste 5.00% Optimiste 12.00% 8.00% mwWw Rendement espr (%) Probabilit 30% 60% 10% Pessimiste Raliste Optimiste WWWWWWWWW WAVAANANA www 5.00% 8.00% 12.00% Rendement espr (%) Probabilit 30% 60% 10% 12.00% Rendement espr (%) cart-type du rendement en (%) 1.8000% Raliste WAWA w Pessimiste 5.00% Optimiste 12.00% 8.00% mwWw Rendement espr (%) Probabilit 30% 60% 10% Pessimiste Raliste Optimiste WWWWWWWWW WAVAANANA www 5.00% 8.00% 12.00% Rendement espr (%) Probabilit 30% 60% 10% 12.00% Rendement espr (%) cart-type du rendement en (%) 1.8000%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock