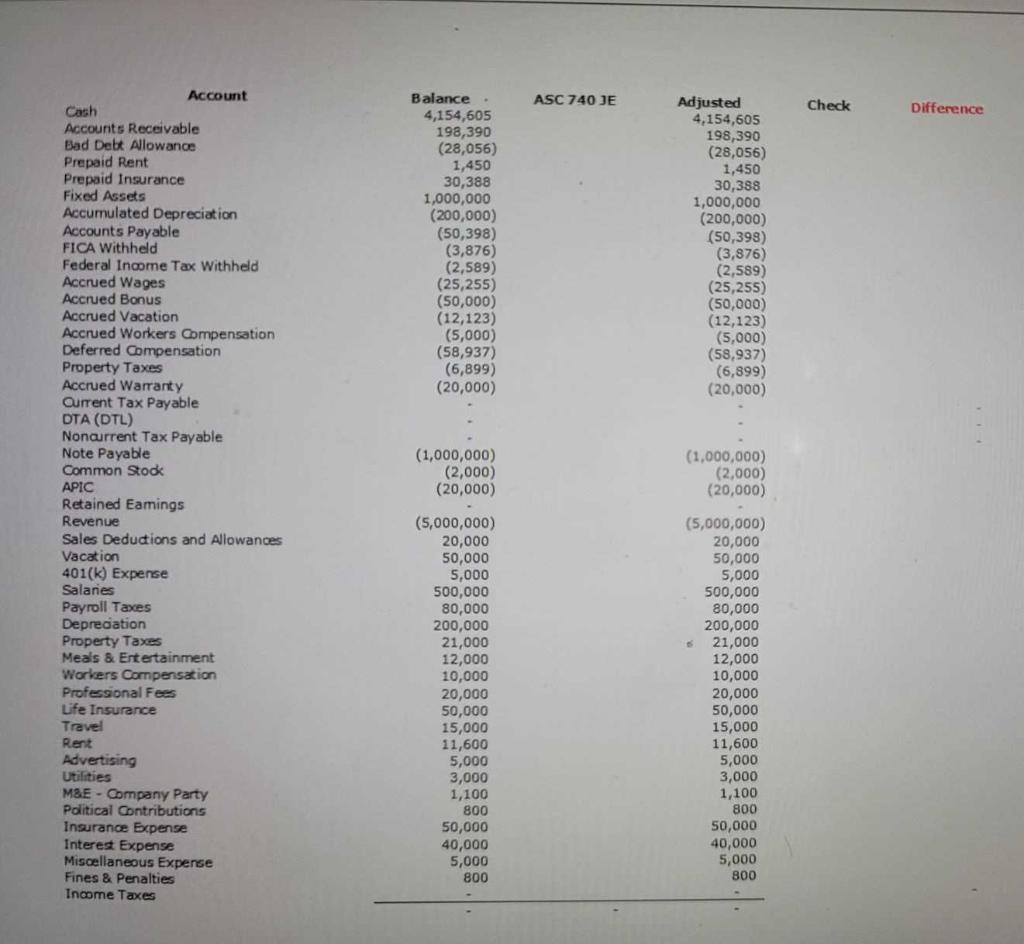

The taxpayer is an accrual method taxpayer. The federal tax rate is 21%. Taxpayer operates in one

Question:

The taxpayer is an accrual method taxpayer.

The federal tax rate is 21%.

Taxpayer operates in one state, State A, which has a tax rate of 4%.

State A apportionment rate is 100%.

Taxpayer's operations generate a $100,000 FDII deduction.

Meals & Entertainment were subject to 50% disallowance.

Penalties were paid to the local government.

Federal depreciation is $400,000.

State A depreciation is $100,000.

Prepaid insurance is for a contract benefit period of 12 months, beginning January 1 of Year 2. Payment was made on December 1 of Year 1.

Accrued Vacation paid out by March 15 of Year 2 is $2,000.

Accrued Bonus paid out by March 15 of Year 2 is $10,000. However, the company deducts the Accrued Bonus as accrued.

The company does not addback life insurance premiums on their tax return or tax provision.

Prepare the income tax provision.

Expert Answer:

Income Tax Provision Taxable income before FDII 100000 FDII deduction 50000 Meals Entertainment disa... View the full answer

Federal Taxation 2016 Comprehensive

ISBN: 9780134104379

29th edition

Authors: Thomas R. Pope, Timothy J. Rupert, Kenneth E. Anderson