Question: Prepare an income statement for the Case Study. Cases 46 manufactures and distributes several varieties of potato chips to three different types of retail accounts:

Prepare an income statement for the Case Study.

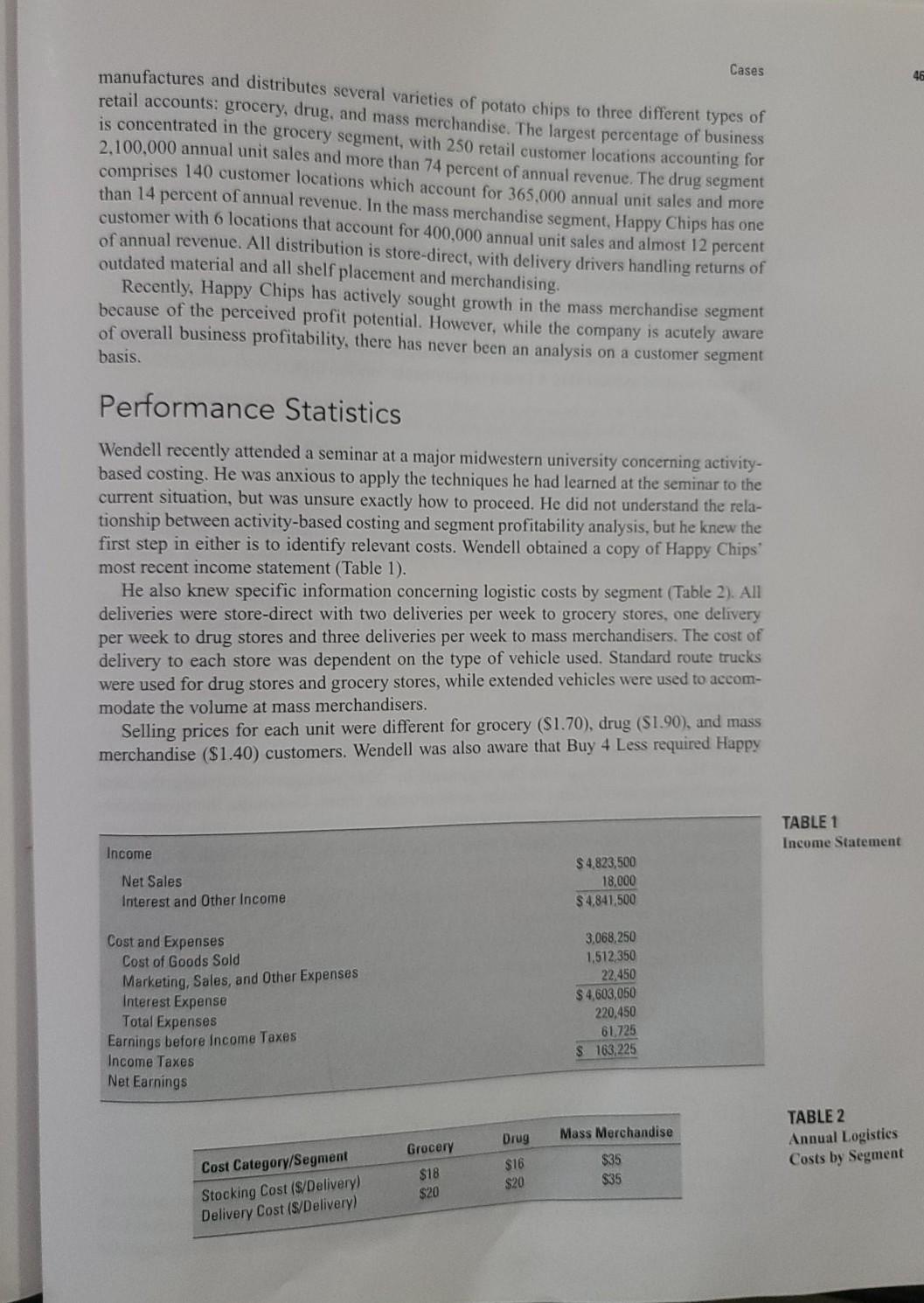

Cases 46 manufactures and distributes several varieties of potato chips to three different types of retail accounts: grocery, drug, and mass merchandise. The largest percentage of business is concentrated in the grocery segment, with 250 retail customer locations accounting for 2,100,000 annual unit sales and more than 74 percent of annual revenue. The drug segment comprises 140 customer locations which account for 365.000 annual unit sales and more than 14 percent of annual revenue. In the mass merchandise segment, Happy Chips has one customer with 6 locations that account for 400,000 annual unit sales and almost 12 percent of annual revenue. All distribution is store-direct, with delivery drivers handling returns of outdated material and all shelf placement and merchandising. Recently, Happy Chips has actively sought growth in the mass merchandise segment because of the perceived profit potential. However, while the company is acutely aware of overall business profitability, there has never been an analysis on a customer segment basis. Performance Statistics Wendell recently attended a seminar at a major midwestern university concerning activity- based costing. He was anxious to apply the techniques he had learned at the seminar to the current situation, but was unsure exactly how to proceed. He did not understand the rela- tionship between activity-based costing and segment profitability analysis, but he knew the first step in either is to identify relevant costs. Wendell obtained a copy of Happy Chips' most recent income statement (Table 1). He also knew specific information concerning logistic costs by segment (Table 2). All deliveries were store-direct with two deliveries per week to grocery stores, one delivery per week to drug stores and three deliveries per week to mass merchandisers. The cost of delivery to each store was dependent on the type of vehicle used. Standard route trucks were used for drug stores and grocery stores, while extended vehicles were used to accom- modate the volume at mass merchandisers. Selling prices for each unit were different for grocery ($1.70), drug (51.90), and mass merchandise ($1.40) customers. Wendell was also aware that Buy 4 Less required Happy TABLE 1 Income Statement Income Net Sales Interest and Other Income $ 4,823,500 18,000 $4,841,500 Cost and Expenses Cost of Goods Sold Marketing, Sales, and Other Expenses Interest Expense Total Expenses Earnings before Income Taxes Income Taxes Net Earnings 3,068,250 1,512, 350 22.450 $4,603,050 220,450 61725 $ 163,225 Drug Mass Merchandise TABLE 2 Annual Logistics Costs by Segment Grocery $16 $20 $18 $20 $35 $35 Cost Category/Segment Stocking Cost (S/Delivery) Delivery Cost (S/Delivery) Cases Chips to cover the suggested retail price (generally about $3.00 per unit regardless of chan- nel) with a sticker bearing its reduced price. The machinery required to apply these labels had an annual lease cost of $40,000,00. Labor and materials ant an additional $6 per unit Conclusion As Wendell sat in his office compiling information to complete the segment profitability analysis, he received several unsolicited offers for assistance. Bill Smith, manager of mar- keting, urged him not to bother with the analysis: Buy 4 Less is clearly our single most important customer. Look at the sales per store. We should immediately implement the suggested changes. Steve Brown, director of manufacturing, disagreed. He felt the additional manufactur- ing cost required to meet Buy 4 Less's requirements was too high: We should let Buy 4 Less know what we really think about their special requirements. Stick- ers, of all things! What business do they think we are in? The sales force had a different opinion. Jake Williams felt the grocery segment was most important: Just look at that volume! How could they be anything but our best customers? The broad interest being generated by this assignment worried Wendell. Would he have to justify his recommendations to everyone in the company? Wendell quietly closed his office door. Based on the available information and his own knowledge of ABC systems, Wendell Worthmann needed to complete a segment profitability analysis and associated spread- sheet before his meeting with Harold in the morning. With all these interruptions, it was going to be a long night

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock