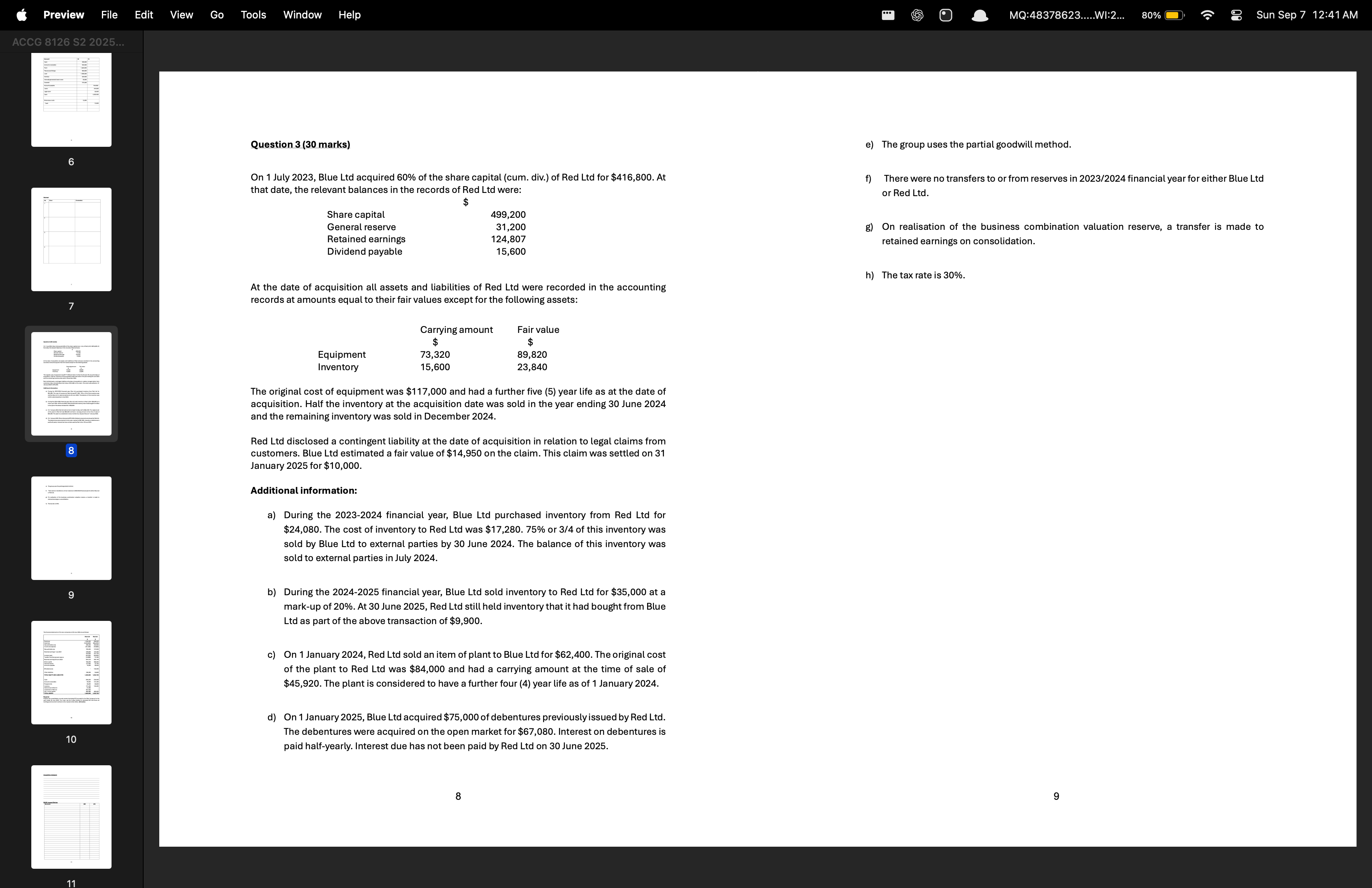

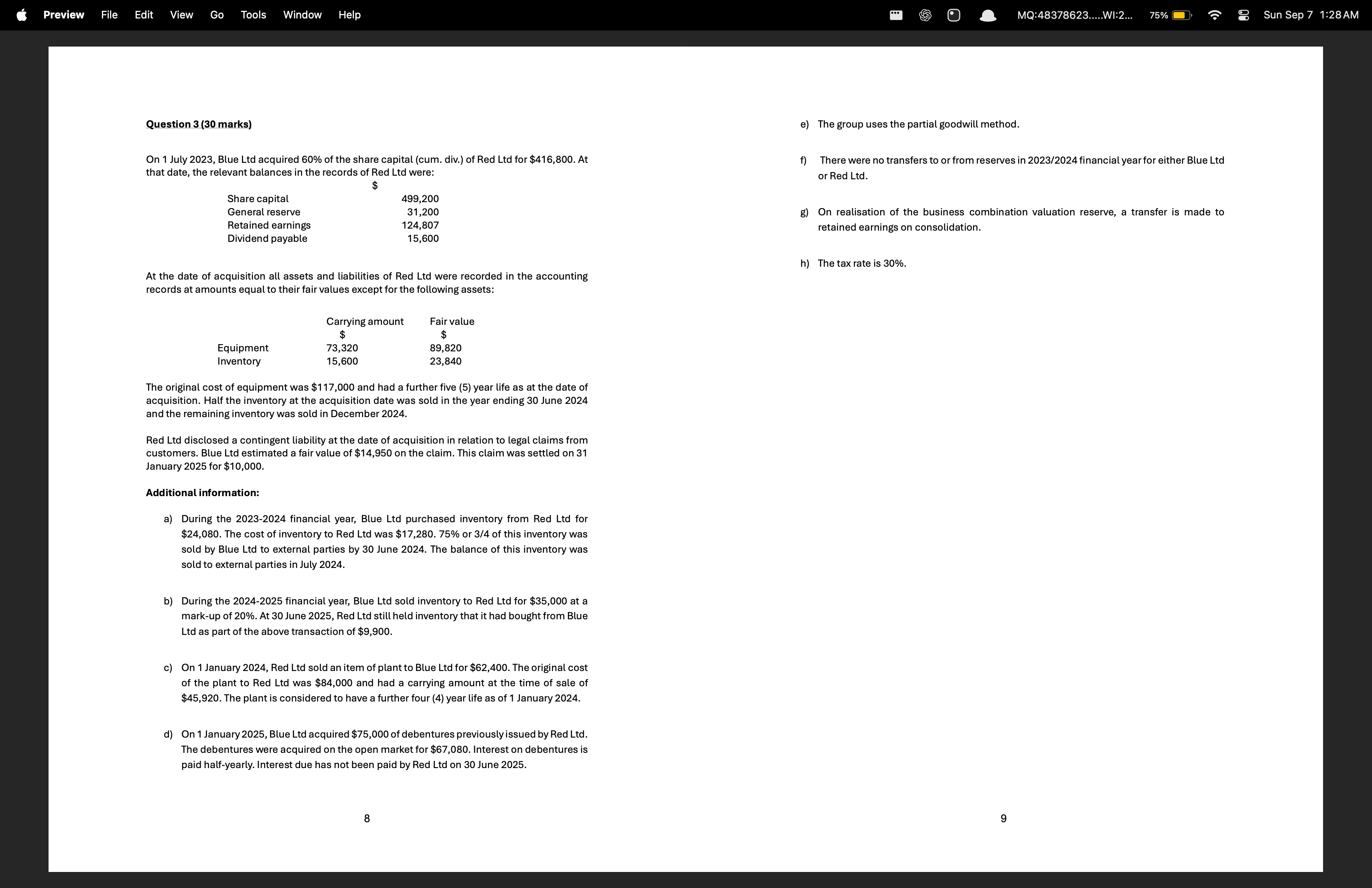

Question: @ Preview File Edit View Go Tools Window Help iS (7) , Y MQ:4837862: lA] eo a VSC A Question 3 (30 marks) The group

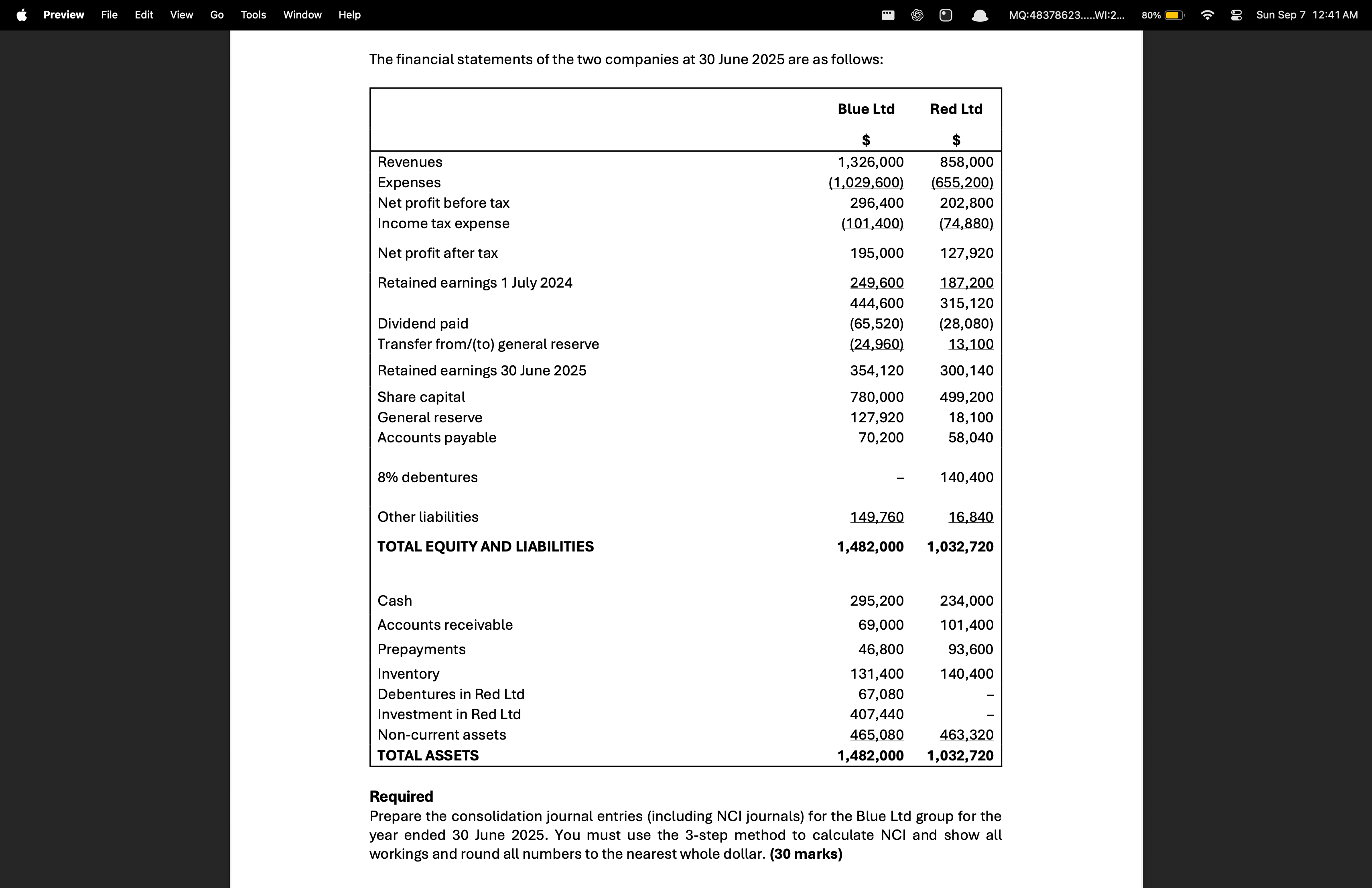

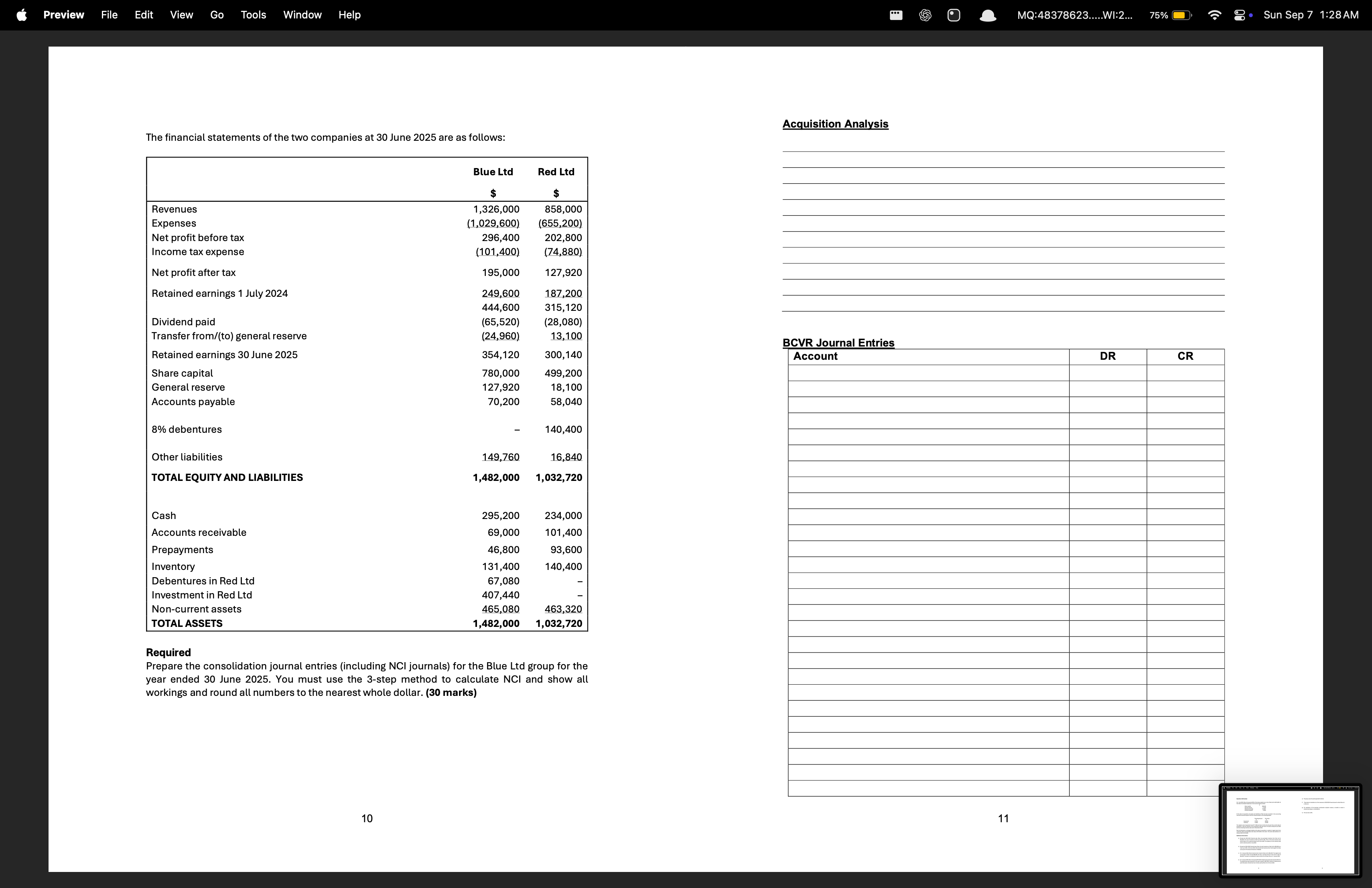

@ Preview File Edit View Go Tools Window Help iS (7) , Y MQ:4837862: lA] eo a VSC A Question 3 (30 marks) The group uses the partial goodwill method. On 1 July 2023, Blue Ltd acquired 60% of the share capital (cum. div.) of Red Ltd for $416,800. At There were no transfers to or from reserves in 2023/2024 financial year for either Blue Ltd that date, the relevant balances in the records of Red Ltd were: or Red Ltd. $ Share capital 499,200 General reserve 31,200 On realisation of the business combination valuation reserve, a transfer is made to Retained earnings 124,807 retained earnings on consolidation. Dividend payable 15,600 The tax rate is 30%. At the date of acquisition all assets and liabilities of Red Ltd were recorded in the accounting records at amounts equal to their fair values except for the following assets: Carryingamount _Fair value $ $ Equipment 73,320 89,820 Inventory 15,600 23,840 The original cost of equipment was $117,000 and had a further five (5) year life as at the date of acquisition. Half the inventory at the acquisition date was sold in the year ending 30 June 2024 and the remaining inventory was sold in December 2024. Red Ltd disclosed a contingent liability at the date of acquisition in relation to legal claims from customers. Blue Ltd estimated a fair value of $14,950 on the claim. This claim was settled on 31 January 2025 for $10,000. Additional information: a) During the 2023-2024 financial year, Blue Ltd purchased inventory from Red Ltd for $24,080. The cost of inventory to Red Ltd was $17,280. 75% or 3/4 of this inventory was sold by Blue Ltd to external parties by 30 June 2024. The balance of this inventory was sold to external parties in July 2024. During the 2024-2025 financial year, Blue Ltd sold inventory to Red Ltd for $35,000 at a mark-up of 20%. At 30 June 2025, Red Ltd still held inventory that it had bought from Blue Ltd as part of the above transaction of $9,900. On 1 January 2024, Red Ltd sold an item of plant to Blue Ltd for $62,400. The original cost of the plant to Red Ltd was $84,000 and had a carrying amount at the time of sale of $45,920. The plant is considered to have a further four (4) year life as of 1 January 2024. On1 January 2025, Blue Ltd acquired $75,000 of debentures previously issued by Red Ltd. The debentures were acquired on the open market for $67,080. Interest on debentures is paid half-yearly. Interest due has not been paid by Red Ltd on 30 June 2025. 6 i 8 9 10 Preview File Edit View Go Tools Window MQ:48378623.....WI:2... 80% Sun Sep 7 12:41 AM The financial statements of the two companies at 30 June 2025 are as follows: Blue Ltd Red Ltd $ Revenues 1,326,000 858,000 Expenses (1,029,600) (655,200) Net profit before tax 296,400 202,800 Income tax expense (101,400) (74,880) rofit after tax 195,000 127,920 Retained earnings 1 July 2024 249,600 187,200 444,600 315, 120 Dividend paid (65,520) (28,080) Transfer from/(to) general reserve (24,960) 13,100 Retained earnings 30 June 2025 354, 120 300, 140 Share capital 780,000 499,200 General reserve 127,920 18, 100 Accounts payable 70,200 58,040 8% debentures 140,400 Other liabilities 149,760 16,840 TOTAL EQUITY AND LIABILITIES 1,482,000 1,032,720 Cash 295,200 234,000 Accounts receivable 69,000 101,400 Prepayments 46,800 93,600 Inventory 131,400 140,400 Debentures in Red Ltd 67,080 Investment in Red Ltd 407,440 Non-current assets 465,080 463,320 TOTAL ASSETS 1,482,000 1,032,720 Required Prepare the consolidation journal entries (including NCI journals) for the Blue Ltd group for the year ended 30 June 2025. You must use the 3-step method to calculate NCI and show all workings and round all numbers to the nearest whole dollar. (30 marks)3 eT aS Edit View Go Tools Window' Help Question 3 (30 marks) On 1 July 2023, Blue Ltd acquired 60% of the share capital (cum. div.) of Red Ltd for $416,800. At that date, the relevant balances in the records of Red Ltd were: $ Share capital 499,200 General reserve 31,200 Retained earnings 124,807 Dividend payable 15,600 At the date of acquisition all assets and liabilities of Red Ltd were recorded in the accounting records at amounts equal to their fair values except for the following assets: Carrying amount Fair value $ Equipment 73,320 89,820 Inventory 15,600 23,840 The original cost of equipment was $117,000 and had a further five (5) year life as at the date of acquisition. Half the inventory at the acquisition date was sold in the year ending 30 June 2024 and the remaining inventory was sold in December 2024. Red Ltd disclosed a contingent liability at the date of acquisition in relation to legal claims from customers. Blue Ltd estimated a fair value of $14,950 on the claim. This claim was settled on 31 January 2025 for $10,000. Additional information: a) During the 2023-2024 financial year, Blue Ltd purchased inventory from Red Ltd for $24,080. The cost of inventory to Red Ltd was $17,280. 75% or 3/4 of this inventory was sold by Blue Ltd to external parties by 30 June 2024. The balance of this inventory was sold to external parties in July 2024. During the 2024-2025 financial year, Blue Ltd sold inventory to Red Ltd for $35,000 at a mark-up of 20%. At 30 June 2025, Red Ltd still held inventory that it had bought from Blue Ltd as part of the above transaction of $9,900. On 1 January 2024, Red Ltd sold an item of plant to Blue Ltd for $62,400. The original cost of the plant to Red Ltd was $84,000 and had a carrying amount at the time of sale of $45,920. The plant is considered to have a further four (4) year life as of 1 January 2024. On 1 January 2025, Blue Ltd acquired $75,000 of debentures previously issued by Red Ltd. The debentures were acquired on the open market for $67,080. Interest on debentures is paid half-yearly. Interest due has not been paid by Red Ltd on 30 June 2025. @ MQ:48378623....Wi:2... 75 The group uses the partial goodwill method. There were no transfers to or from reserves in 2023/2024 financial year for either Blue Ltd or Red Ltd. On realisation of the business combination valuation reserve, a transfer is made to retained earnings on consolidation. The tax rate is 30%. Sun Sep 7 1:28AM CC eS eC Co) cs) N32 Sun Sep 7 1:28AM The financial statements of the two companies at 30 June 2025 are as follows: Blue Ltd Red Ltd $ $ Revenues 1,326,000 858,000 Expenses (1,029,600) (655,200) Net profit before tax 296,400 202,800 Income tax expense (101,400) (74,880) Net profit after tax 195,000 127,920 Retained earnings 1 July 2024 249,600 187,200 444,600 315,120 Dividend paid (65,520) (28,080) Transfer from/(to) general reserve (24,960) 13,100 BCVR Journal Entries Retained earnings 30 June 2025 354,120 300,140 Account Share capital 780,000 499,200 General reserve 127,920 18,100 Accounts payable 70,200 58,040 8% debentures 140,400 Other liabilities 149,760 16,840 TOTAL EQUITY AND LIABILITIES 1,482,000 1,032,720 Cash 295,200 234,000 Accounts receivable 69,000 101,400 Prepayments 46,800 93,600 Inventory 131,400 140,400 Debentures in Red Ltd 67,080 a Investment in Red Ltd 407,440 - Non-current assets 465,080 463,320 TOTAL ASSETS 1,482,000 1,032,720 Required Prepare the consolidation journal entries (including NCI journals) for the Blue Ltd group for the year ended 30 June 2025. You must use the 3-step method to calculate NCI and show all workings and round all numbers to the nearest whole dollar. (30 marks) Preview File Edit View Go Tools Window Help O MQ:48378623.....WI:2... 75% 8 . Sun Sep 7 1:28 AM Intra-group Journal Entries Account DR CR Pre-Acquisition Journal Entries Account DR CR 12 13Preview File Edit View Go Tools Window Help O MQ:48378623.....WI:2... 75% . Sun Sep 7 1:28 AM NCI Journal Entries (Workings on the next page) Step 2 workings Account DR CR Opening RE: less pre-acq. RE: Post acq RE: Adjustments Adj. post acq. RE: NCI allocation Step 3 workings Current year profit Adjustments Adj. profit: NCI allocation 14 15

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!