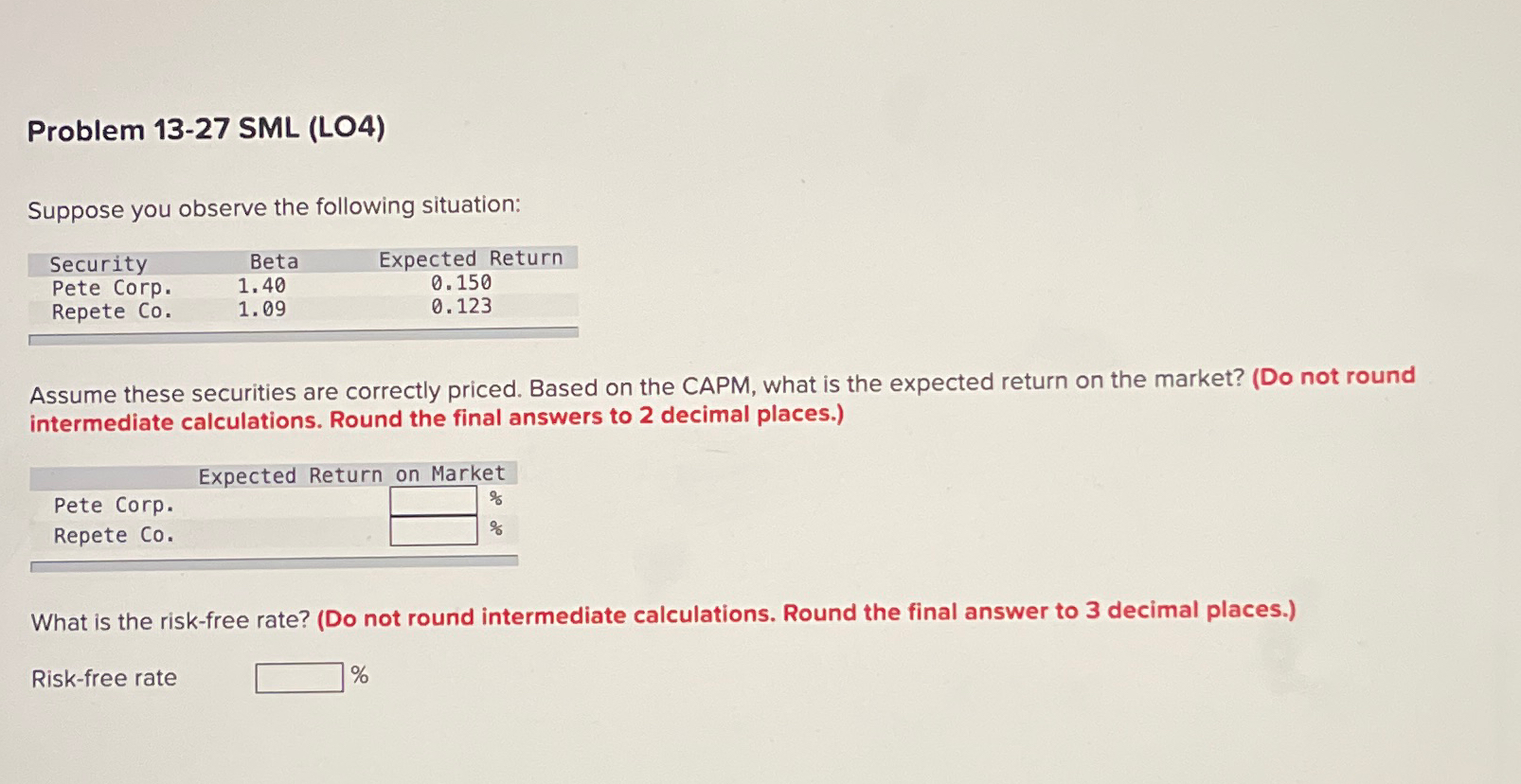

Question: Problem 1 3 - 2 7 SML ( LO 4 ) Suppose you observe the following situation: table [ [ Security , Beta,Expected Return

Problem SML LO

Suppose you observe the following situation:

tableSecurityBeta,Expected ReturnPete Corp.,Repete Co

Assume these securities are correctly priced. Based on the CAPM, what is the expected return on the market? Do not round intermediate calculations. Round the final answers to decimal places.

tablePete Corp.,Expected Return on MarketRepete Co

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock