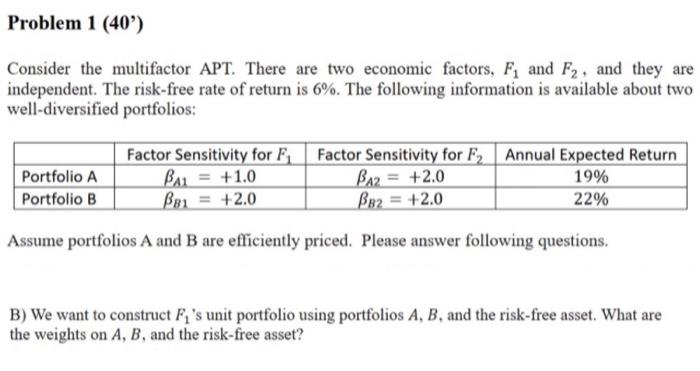

Question: Problem 1 (40') Consider the multifactor APT. There are two economic factors, F, and F2, and they are independent. The risk-free rate of return is

Problem 1 (40') Consider the multifactor APT. There are two economic factors, F, and F2, and they are independent. The risk-free rate of return is 6%. The following information is available about two well-diversified portfolios: Portfolio A Portfolio B Factor Sensitivity for F Factor Sensitivity for F, Annual Expected Return Bar = +1.0 BA2 = +2.0 19% Bai = +2.0 BB2 = +2.0 22% Assume portfolios A and B are efficiently priced. Please answer following questions, B) We want to construct Fi's unit portfolio using portfolios A, B, and the risk-free asset. What are the weights on A, B, and the risk-free asset

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock