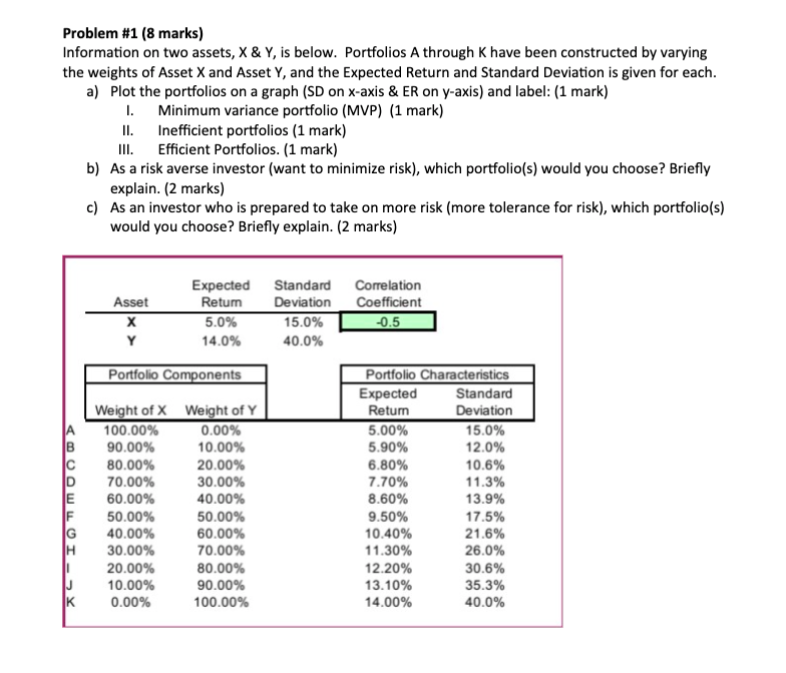

Question: Problem #1 (8 marks) Information on two assets, X & Y, is below. Portfolios A through K have been constructed by varying the weights of

Problem #1 (8 marks) Information on two assets, X & Y, is below. Portfolios A through K have been constructed by varying the weights of Asset X and Asset Y, and the Expected Return and Standard Deviation is given for each. a) Plot the portfolios on a graph (SD on x-axis & ER on y-axis) and label: (1 mark) 1. Minimum variance portfolio (MVP) (1 mark) II. Inefficient portfolios (1 mark) III. Efficient Portfolios. (1 mark) b) As a risk averse investor (want to minimize risk), which portfolio(s) would you choose? Briefly explain. (2 marks) c) As an investor who is prepared to take on more risk (more tolerance for risk), which portfolio(s) would you choose? Briefly explain. (2 marks) Expected Standard Asset Retum Deviation X 5.0% 15.0% Y 14.0% 40.0% Portfolio Components Correlation Coefficient -0.5 A | C D LE Portfolio Characteristics Expected Standard Return Deviation 5.00% 15.0% 5.90% 12.0% 6.80% 10.6% 7.70% 11.3% 8.60% 13.9% 9.50% 17.5% 10.40% 21.6% 11.30% 26.0% 12.20% 30.6% 13.10% 35.3% 14.00% 40.0% Weight of X Weight of Y 100.00% 0.00% 90.00% 10.00% 80.00% 20.00% 70.00% 30.00% 60.00% 40.00% 50.00% 50.00% 40.00% 60.00% 30.00% 70.00% 20.00% 80.00% 10.00% 90.00% 0.00% 100.00% ULUI-X 1 J K

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts