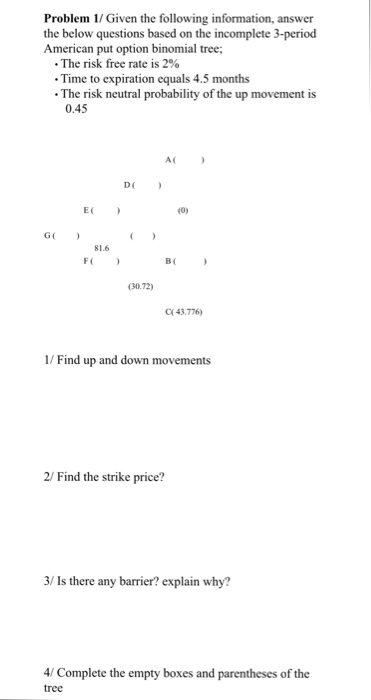

Question: Problem 1/ Given the following information, answer the below questions based on the incomplete 3-period American put option binomial tree The risk free rate is

Problem 1/ Given the following information, answer the below questions based on the incomplete 3-period American put option binomial tree The risk free rate is 2% Time to expiration equals 4.5 months The risk neutral probability of the up movement is 0.45 AC DC EC GC 81.6 B( (30.72) 43.776) 1/ Find up and down movements 2/ Find the strike price? 3/ Is there any barrier? explain why? 4/ Complete the empty boxes and parentheses of the tree Problem 1/ Given the following information, answer the below questions based on the incomplete 3-period American put option binomial tree The risk free rate is 2% Time to expiration equals 4.5 months The risk neutral probability of the up movement is 0.45 AC DC EC GC 81.6 B( (30.72) 43.776) 1/ Find up and down movements 2/ Find the strike price? 3/ Is there any barrier? explain why? 4/ Complete the empty boxes and parentheses of the tree

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts