Question: Problem 1 In the table below, you see the data on four Wal-Mart call options, recorded on 4/13/20. All options expire May 1, 2020. The

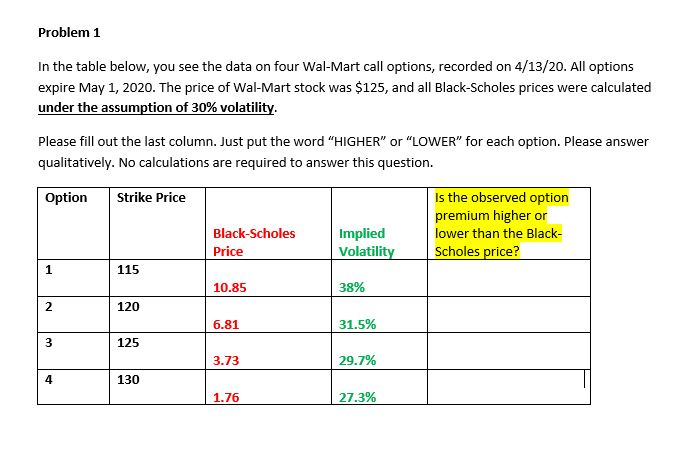

Problem 1 In the table below, you see the data on four Wal-Mart call options, recorded on 4/13/20. All options expire May 1, 2020. The price of Wal-Mart stock was $125, and all Black-Scholes prices were calculated under the assumption of 30% volatility Please fill out the last column. Just put the word "HIGHER" or "LOWER" for each option. Please answer qualitatively. No calculations are required to answer this question. Option Strike Price Black-Scholes Price Is the observed option premium higher or lower than the Black- Scholes price? Implied Volatility 10.85 38% 120 6.81 31.5% 125 3.73 29.7% 130 1.76 27.3%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock