Question: Problem 1: Please explain and show your work. A mutual fund manager has a $40 million portfolio with a beta of 1.00. The risk-free rate

Problem 1: Please explain and show your work.

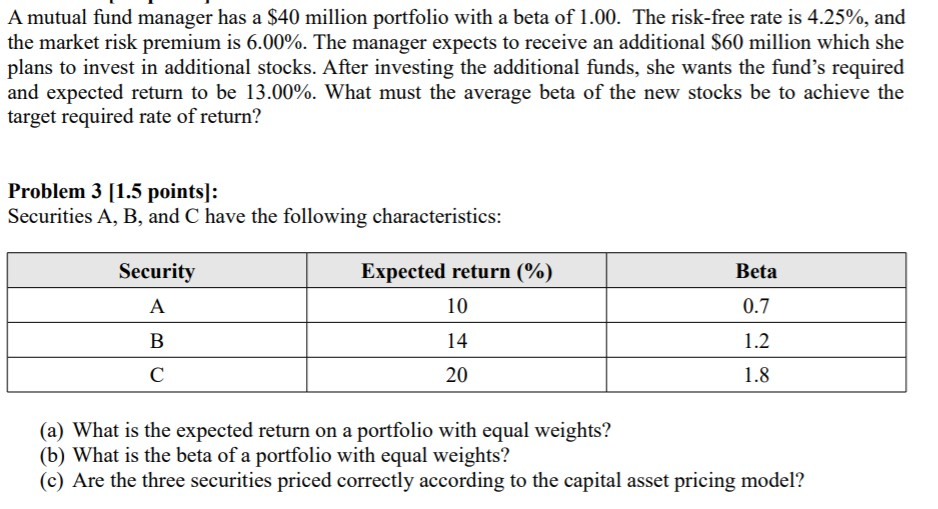

A mutual fund manager has a $40 million portfolio with a beta of 1.00. The risk-free rate is 4.25%, and the market risk premium is 6.00%. The manager expects to receive an additional $60 million which she plans to invest in additional stocks. After investing the additional funds, she wants the fund's required and expected return to be 13.00%. What must the average beta of the new stocks be to achieve the target required rate of return? Problem 3 (1.5 points]: Securities A, B, and C have the following characteristics: Security Expected return (%) Beta 0.7 10 14 1.2 20 1.8 (a) What is the expected return on a portfolio with equal weights? (b) What is the beta of a portfolio with equal weights? (c) Are the three securities priced correctly according to the capital asset pricing model

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts