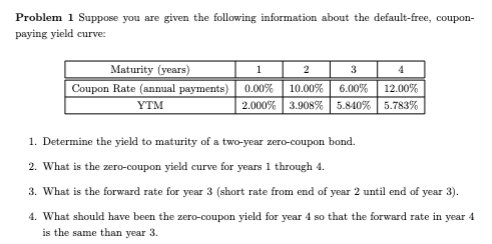

Question: Problem 1 Suppose you are given the following information about the default-free, couponpaying yield curve: 1. Determine the yield to maturity of a two-year zero-coupon

Problem 1 Suppose you are given the following information about the default-free, couponpaying yield curve: 1. Determine the yield to maturity of a two-year zero-coupon bond. 2. What is the zero-coupon yield curve for years 1 through 4 . 3. What is the forward rate for year 3 (short rate from end of year 2 until end of year 3). 4. What should have been the zero-coupon yield for year 4 so that the forward rate in year 4 is the same than year 3 . Problem 1 Suppose you are given the following information about the default-free, couponpaying yield curve: 1. Determine the yield to maturity of a two-year zero-coupon bond. 2. What is the zero-coupon yield curve for years 1 through 4 . 3. What is the forward rate for year 3 (short rate from end of year 2 until end of year 3). 4. What should have been the zero-coupon yield for year 4 so that the forward rate in year 4 is the same than year 3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts