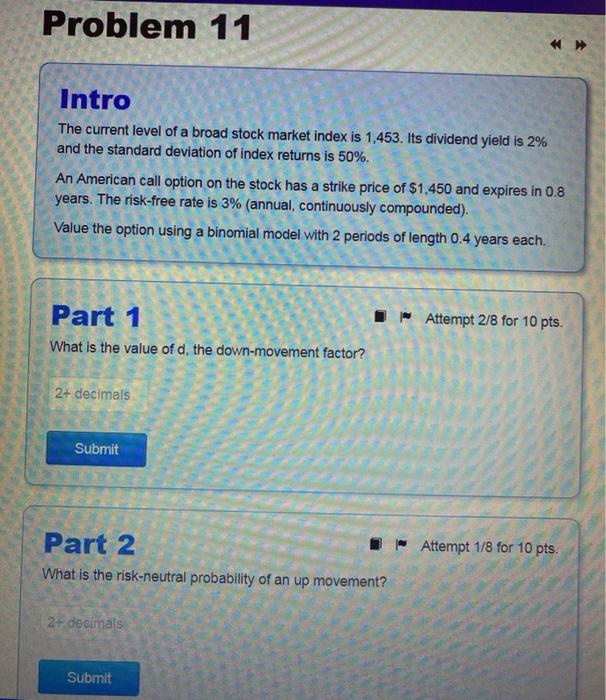

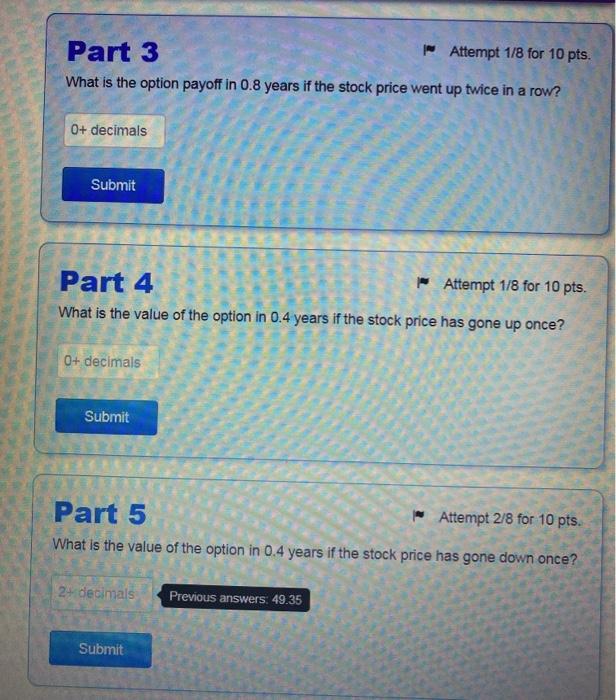

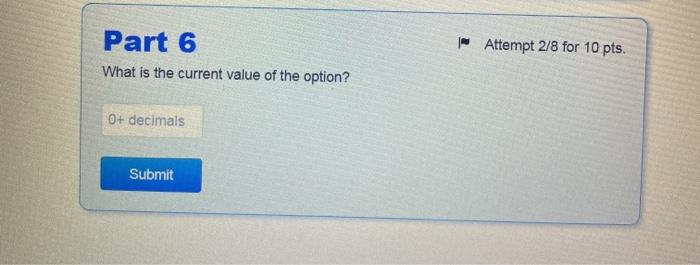

Question: Problem 11 Intro The current level of a broad stock market index is 1,453. Its dividend yield is 2% and the standard deviation of index

Problem 11 Intro The current level of a broad stock market index is 1,453. Its dividend yield is 2% and the standard deviation of index returns is 50%. An American call option on the stock has a strike price of $1.450 and expires in 0.8 years. The risk-free rate is 3% (annual, continuously compounded). Value the option using a binomial model with 2 periods of length 0.4 years each. Attempt 2/8 for 10 pts. Part 1 What is the value of d, the down-movement factor? 2+ decimals Submit Attempt 1/8 for 10 pts. Part 2 What is the risk-neutral probability of an up movement? 2+ decimals Submit Part 3 | Attempt 1/8 for 10 pts. What is the option payoff in 0.8 years if the stock price went up twice in a row? 0+ decimals Submit Part 4 Attempt 1/8 for 10 pts. What is the value of the option in 0.4 years if the stock price has gone up once? 0+ decimals Submit Part 5 Attempt 2/8 for 10 pts. What is the value of the option in 0.4 years if the stock price has gone down once? 27 decimals Previous answers, 49.35 Submit - Attempt 2/8 for 10 pts. Part 6 What is the current value of the option? 0+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts