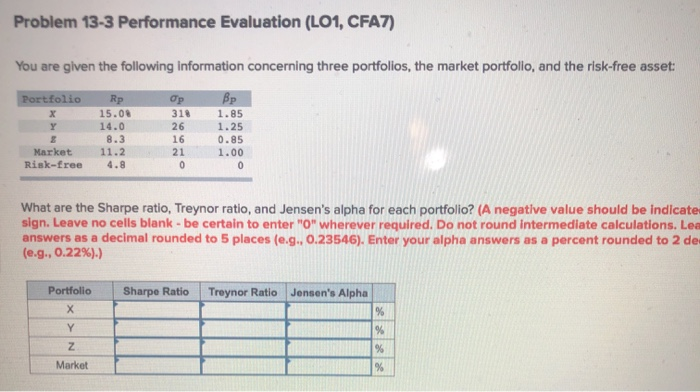

Question: Problem 13-3 Performance Evaluation (L01, CFA7) You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio op Rp

Problem 13-3 Performance Evaluation (L01, CFA7) You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio op Rp 15.08 14.0 8.3 11.2 318 26 1.85 1.25 0.85 1.00 16 21 Market Risk-free What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicate sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Lea answers as a decimal rounded to 5 places (e.g., 0.23546). Enter your alpha answers as a percent rounded to 2 de (e.g., 0.22%).) Portfolio Sharpe Ratio Treynor Ratio Jensen's Alpha Market

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts