Question: Problem 14-4 THIS IS THE ENTIRE PROBLEM. THE THINGS THAT ARE IN BOLD NEED TO BE ANSWERED. I INCLUDED A PICTURE OF WHAT I HAVE

Problem 14-4

THIS IS THE ENTIRE PROBLEM. THE THINGS THAT ARE IN BOLD NEED TO BE ANSWERED. I INCLUDED A PICTURE OF WHAT I HAVE DONE MYSELF. PLEASE HELP. EVERYTHING ELSE IS JUST THERE TO HELP YOU.

Bonds Issued at a Discount and a PremiumEffective Interest Method

Yacuma Corporation issued bonds twice during 2014. The transactions were as follows:

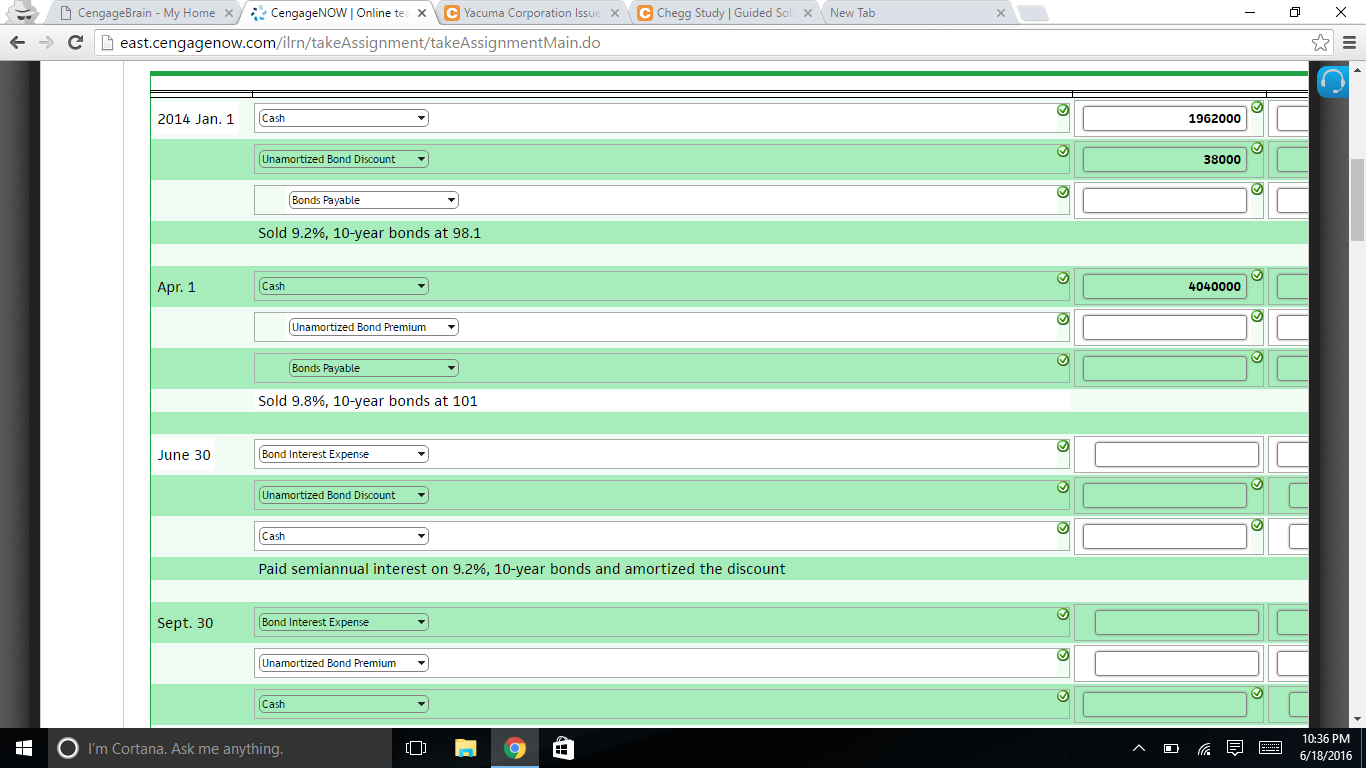

2014 Jan. 1 Issued $2,000,000 of 9.2 percent, 10-year bonds dated January 1, 2014, with interest payable on June 30 and December 31. The bonds were sold at 98.1, resulting in an effective interest rate of 9.5 percent. Apr. 1 Issued $4,000,000 of 9.8 percent, 10-year bonds dated April 1, 2014, with interest payable on March 31 and September 30. The bonds were sold at 101, resulting in an effective interest rate of 9.5 percent. June 30 Paid semiannual interest on the January 1 issue and amortized the discount, using the effective interest method. Sept. 30 Paid semiannual interest on the April 1 issue and amortized the premium, using the effective interest method. Dec. 31 Paid semiannual interest on the January 1 issue and amortized the discount, using the effective interest method. 31 Made an end-of-year adjusting entry to accrue interest on the April 1 issue and to amortize half the premium applicable to the second interest period. 2015 Mar. 31 Paid semiannual interest on the April 1 issue and amortized the premium applicable to the second half of the second interest period.

1. Prepare entries in journal form to record the bond transactions. (Round amounts to the nearest dollar.) If an amount box does not require an entry, leave it blank.

1. The following schedule summarizes the transactions for this problem.

$2,000,000, 9.2%, 10 year $4,000,000, 9.8%, 10 year 2014 Jan. 1 issued at 98.1 (discount) April 1 issued at 101 (premium) June 30 Paid semiannual interest and amortize discount Sept. 30 Paid semiannual interest and amortize premium Dec. 31 Paid semiannual interest and amortize discount Dec. 31 End-of-year adjusting entry to accrue interest and amortize premium 2015 Mar. 31 Paid semiannual interest and amortize premium

Bonds Issued at a Discount

A bond issue is the total value of bonds issued at one time. For example, a $1,000,000 bond issue could consist of one thousand $1,000 bonds. The prices of bonds are stated in terms of a percentage of the face value, or principal, of the bonds. A bond issue quoted at 103 means that a $1,000 bond costs $1,035 ($1,000 x 1.035). When a bond sells at exactly 100, it is said to sell at face value (or par value). When it sells below 100, it is said to sell at a discount; above 100, at a premium. For instance, a $1,000 bond quoted at 87.62 would be selling at a discount and would cost the buyer $876.20.

The entry to record the issuance of the bonds at a discount

increases the Cash account with a debit for the amount of the bond issue less the discount increases the Unamortized Bond Discount account with a debit for the amount of discount increases the Bonds Payable account with a credit for the amount of the bond issued

Assets = Liabilities + Owner's Equity

Cash Dr. Cr. Jan. 1 191,889

Unamortized Bond Discount Dr. Cr. Jan. 1 8,111

Bonds Payable Dr. Cr. Jan. 1 200,000

Journal Entry

2014 Dr. Cr. Jan. 1 Cash 191,889 Unamortized Bond Discount 8,111 Bonds Payable 200,000 Sold $200,000 of 7%, 5-year bonds at 95.9445 Face amount of bonds $200,000 Less purchase price of bonds ($200,000 0.959445) 191,889 Unamortized bond discount $ 8,111

Bonds Issued at a Premium

Carrot issues $200,000 of 7 percent, five-year bonds for $208,530 on January 1, 2014, when the market interest rate is 6 percent. This means that investors will purchase the bonds at 104.265 percent of their face value. In this case, the bonds are being issued at a premium because the face interest rate exceeds the market rate for similar investments.

The journal entry to record the bond issuance at a premium

increases the Cash account for the amount of the bond issue plus the premium increases the Unamortized Bond Premium account for the amount of the premium increases the Bonds Payable account for the amount of the bond issue

Effective Interest Method

With this method, the interest expense decreases slightly each period (see the following exhibit, column B) because the amount of the bond premium amortized increases slightly (column D). This occurs because a fixed rate is applied each period to the gradually decreasing carrying value (column A).

A B C D E F Semiannual Interest Period Carrying Value at Beginning of Period Semiannual Interest Expense at 6% to Be Recorded* (3% A) Semiannual Interest Payment to Bondholders (3% $200,000) Amortization of BondPremium (C B) Unamortized Bond Premium at End of Period (E D) Carrying Value at End of Period (A D) 0 $8,530 $208,530 1 $208,530 $6,256 $7,000 $744 7,786 207,786 2 207,786 6,234 7,000 766 7,020 207,020 3 207,020 6,211 7,000 789 6,231 206,231 4 206,231 6,187 7,000 813 5,418 205,418 5 205,418 6,163 7,000 837 4,581 204,581 6 204,581 6,137 7,000 863 3,718 203,718 7 203,718 6,112 7,000 888 2,830 202,830 8 202,830 6,085 7,000 915 1,915 201,915 9 201,915 6,057 7,000 943 972 200,972 10 200,972 6,028** 7,000 972 - 200,000 *Rounded ** Last periods interest expense equals $6,028 ($7,000 $972); it is actually equal to $6,029 ($200,972 0.03) but the difference is because of the cumulative effect of rounding.

Note that the unamortized bond premium (column E) decreases gradually to zero as the carrying value decreases to the face value (column F). To find the amount of premium amortized in any one interest payment period, subtract the effective interest expense (the carrying value times the effective interest rate, column B) from the interest payment (column C). In semiannual interest period 5, for example, the amortization of premium is $837, which is calculated as follows.

Interest Payment - (Carrying Value Interest Rate) = Amortized Premium $7,000 - ($205,418 0.03) = $837

The journal entry to record the bond premium amortized and interest expense using the effective interest method

increases the Bond Interest Expense account with a debit for the amount calculated in column B decreases the Unamortized Bond Premium account with a debit for the amount calculated in column D decreases the Cash account (or increases the Interest Payable account) with a credit for the amount in column C

End-of year Adjusting Entry to Record Interest Expense and Premium Amortization

The interest payable and discount amortization for the six-month period is calculated as follows.

Carrying Value = Face Value + Unamortized Premium $4,000,000 + ? Interest Expense = Carrying Value Market Interest Rate Interest Time Period ? 9.5% 6/12 Interest Payable = Face Value Face Interest Rate Interest Time Period $4,000,000 9.8% 6/12 Discount Amortized = Interest Expense Interest Payable ?

For December 31, 2014

For this particular bond issue, the interest dates are March 31 and September 30. The company's year end is December 31. Therefore, only three months(or ) of the interest expense and interest payable calculated above would be recorded on December 31, 2014. The other half would be recorded on March 31, 2015.

The journal entry to record the bond discount amortized and interest expense

increases the Bond Interest Expense account with a debit (3 months) decreases the Unamortized Bond Discount account with a credit (3 months) increases the Interest Payable account with a credit (3 months)

For March 1, 2015

You should note that the actual payment is for six months of interest. Of this amount, half was recorded as an expense and a liability in 2014.

The journal entry to pay the bondholders and amortize the premium

increases the Bond Interest Expense account with a debit (3 months) decreases the Bond Interest Payable account with a debit (3 months) decreases the Unamortized Bond Premium account with a credit (3 months) decreases the Cash account with a credit (6 months)

2. Describe the effect of the above transactions on profitability and liquidity by answering the following questions.

a. What is the total interest expense in 2014 for each of the bond issues? $

b. What is the total cash paid in 2014 for each of the bond issues? $

c. What differences, if any, do you observe and how do you explain them?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts