Question: Problem 2 (15 points) Now assume that apart from the securities in problem 1, you also have the market portfolio. Consider the following forecasts of

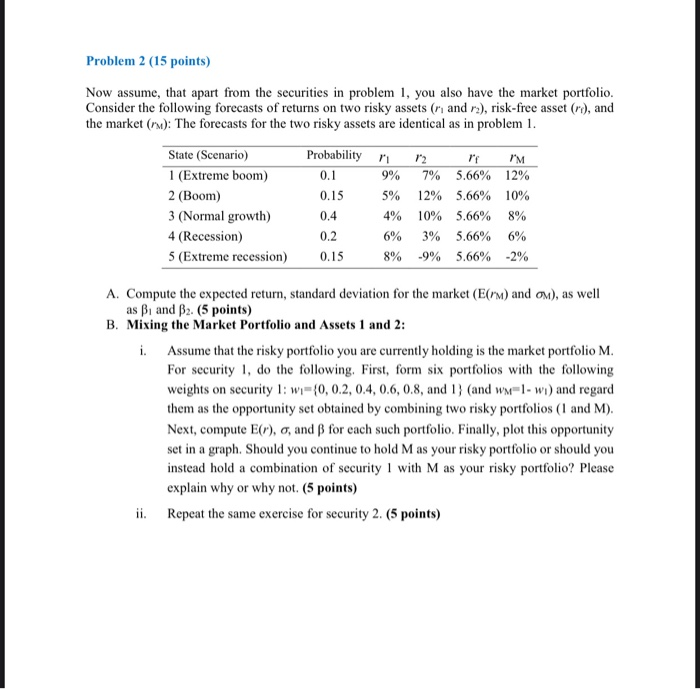

Problem 2 (15 points) Now assume that apart from the securities in problem 1, you also have the market portfolio. Consider the following forecasts of returns on two risky assets (n and r.), risk-free asset (r), and the market (ru): The forecasts for the two risky assets are identical as in problem 1. State (Scenario) Probability 12 1 (Extreme boom) 0.1 9% 7% 5.66% 12% 2 (Boom) 5% 12% 5.66% 10% 3 (Normal growth) 0.4 4% 10% 5.66% 8% 4 (Recession) 0.2 6% 3% 5.66% 6% 5 (Extreme recession) 0.15 8% -9% 5.66% -2% 0.15 A. Compute the expected return, standard deviation for the market (E(rm) and om), as well as B and B2. (5 points) B. Mixing the Market Portfolio and Assets 1 and 2: i. Assume that the risky portfolio you are currently holding is the market portfolio M. For security 1, do the following. First, form six portfolios with the following weights on security 1: W={0,0.2, 0.4, 0.6,0.8, and 1} (and wm-1-wi) and regard them as the opportunity set obtained by combining two risky portfolios (1 and M). Next, compute E(r), o, and B for each such portfolio. Finally, plot this opportunity set in a graph. Should you continue to hold M as your risky portfolio or should you instead hold a combination of security 1 with M as your risky portfolio? Please explain why or why not. (5 points) ii. Repeat the same exercise for security 2. (5 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts