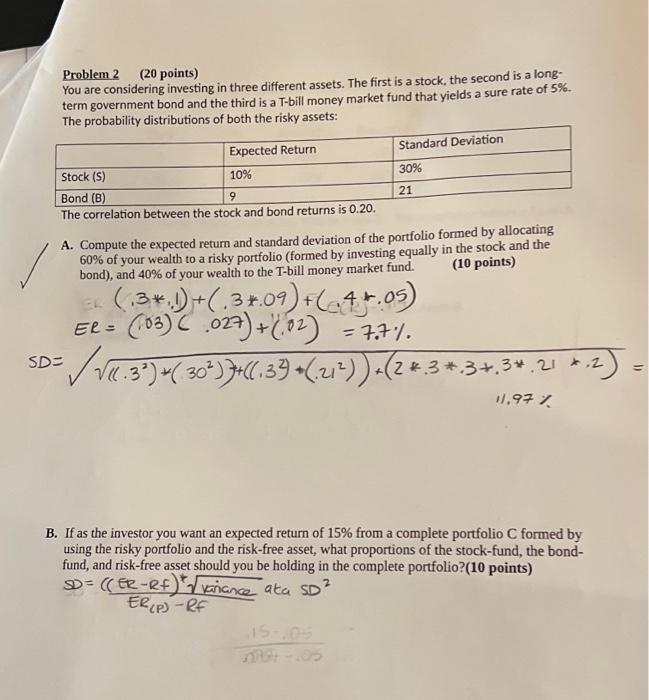

Question: Problem 2 (20 points) You are considering investing in three different assets. The first is a stock, the second is a longterm government bond and

Problem 2 (20 points) You are considering investing in three different assets. The first is a stock, the second is a longterm government bond and the third is a T-bill money market fund that yields a sure rate of 5%. The probability distributions of both the risky assets: The correlation between the stock ana Donu returns is vicu. A. Compute the expected return and standard deviation of the portfolio formed by allocating 60% of your wealth to a risky portfolio (formed by investing equally in the stock and the bond), and 40% of your wealth to the T-bill money market fund. (10 points) (.3.1)+(.3.09)+(.4+.05)ER=(.03)C.027)+(.02)=7.7% D=(1.32)+(302))+((.32)+(.212))+(2.3.3.3.21.2) B. If as the investor you want an expected return of 15% from a complete portfolio C formed by using the risky portfolio and the risk-free asset, what proportions of the stock-fund, the bondfund, and risk-free asset should you be holding in the complete portfolio?(10 points) SD=ER(P)Rf((ERRf)tkarianceataSD2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts