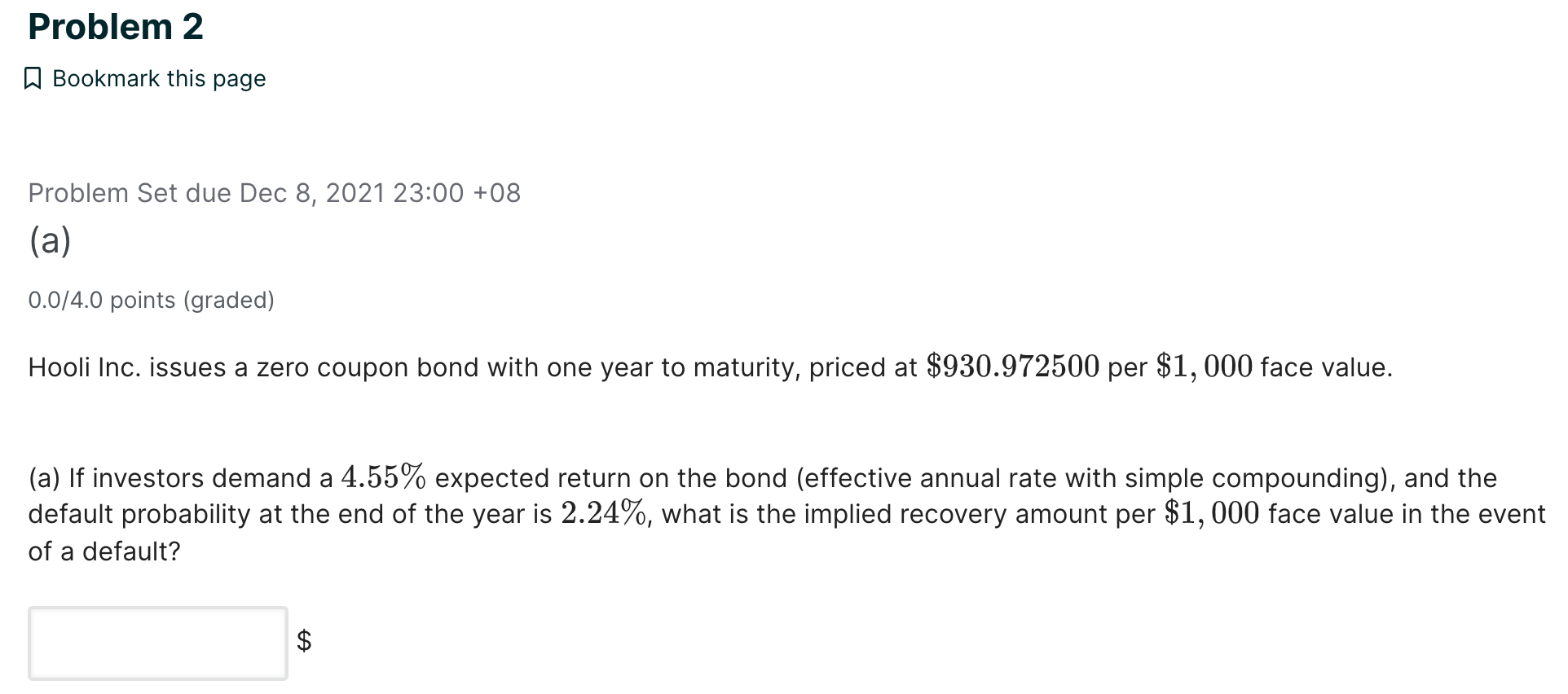

Question: Problem 2 A Bookmark this page Problem Set due Dec 8, 2021 23:00 +08 (a) 0.0/4.0 points (graded) Hooli Inc. issues a zero coupon bond

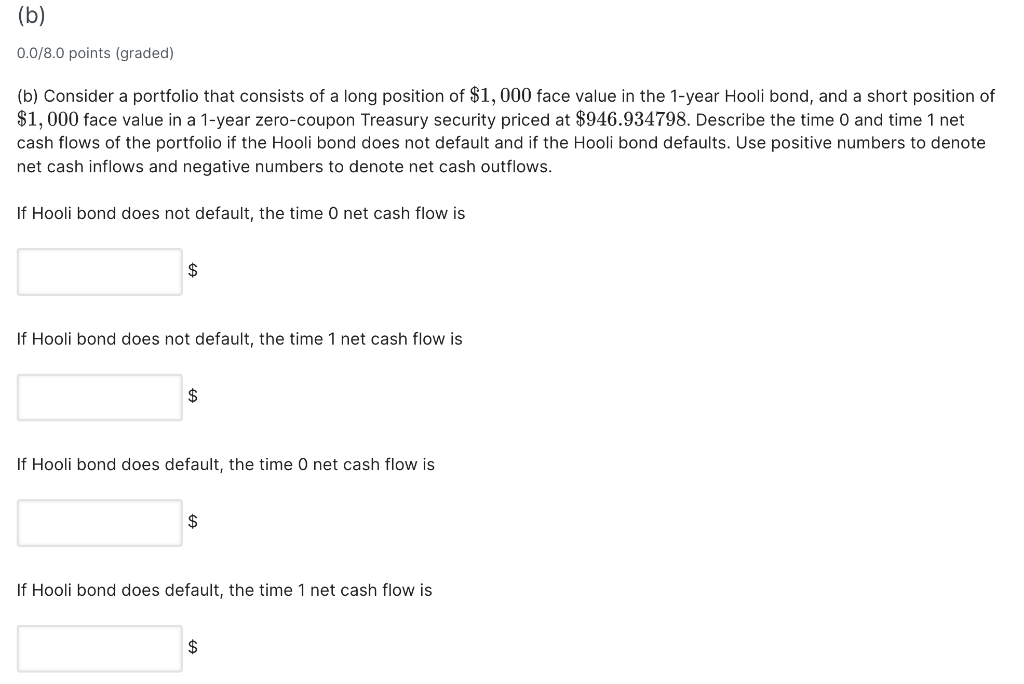

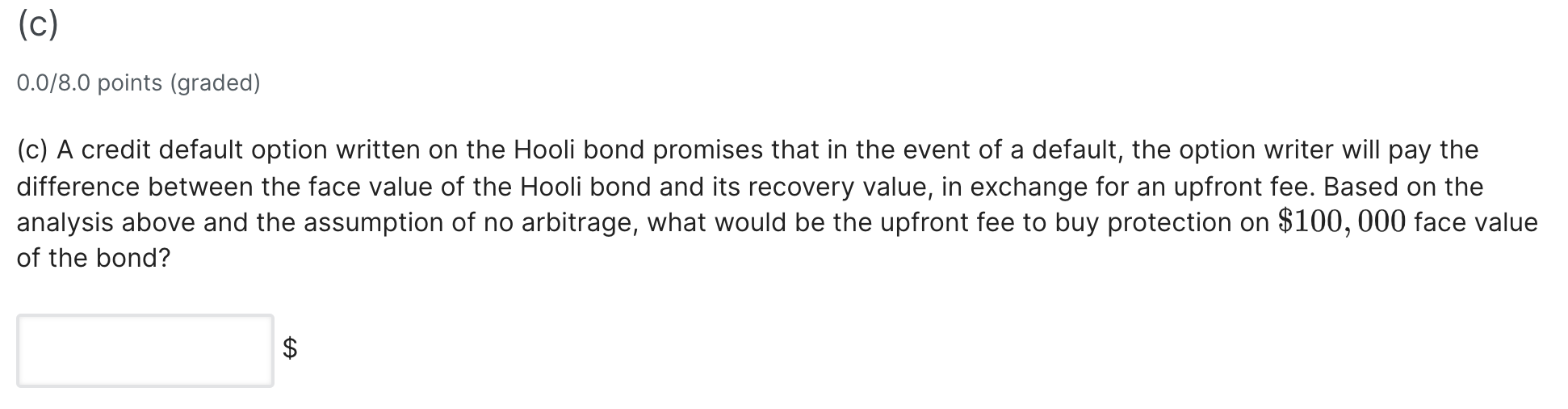

Problem 2 A Bookmark this page Problem Set due Dec 8, 2021 23:00 +08 (a) 0.0/4.0 points (graded) Hooli Inc. issues a zero coupon bond with one year to maturity, priced at $930.972500 per $1,000 face value. a (a) If investors demand a 4.55% expected return on the bond (effective annual rate with simple compounding), and the default probability at the end of the year is 2.24%, what is the implied recovery amount per $1,000 face value in the event of a default? $ (b) 0.0/8.0 points (graded) (b) Consider a portfolio that consists of a long position of $1,000 face value in the 1-year Hooli bond, and a short position of $1,000 face value in a 1-year zero-coupon Treasury security priced at $946.934798. Describe the time 0 and time 1 net cash flows of the portfolio if the Hooli bond does not default and if the Hooli bond defaults. Use positive numbers to denote net cash inflows and negative numbers to denote net cash outflows. If Hooli bond does not default, the time 0 net cash flow is $ If Hooli bond does not default, the time 1 net cash flow is $ If Hooli bond does default, the time 0 net cash flow is $ If Hooli bond does default, the time 1 net cash flow is $ (c) 0.0/8.0 points (graded) (c) A credit default option written on the Hooli bond promises that in the event of a default, the option writer will pay the difference between the face value of the Hooli bond and its recovery value, in exchange for an upfront fee. Based on the analysis above and the assumption of no arbitrage, what would be the upfront fee to buy protection on $100,000 face value of the bond? $ Problem 2 A Bookmark this page Problem Set due Dec 8, 2021 23:00 +08 (a) 0.0/4.0 points (graded) Hooli Inc. issues a zero coupon bond with one year to maturity, priced at $930.972500 per $1,000 face value. a (a) If investors demand a 4.55% expected return on the bond (effective annual rate with simple compounding), and the default probability at the end of the year is 2.24%, what is the implied recovery amount per $1,000 face value in the event of a default? $ (b) 0.0/8.0 points (graded) (b) Consider a portfolio that consists of a long position of $1,000 face value in the 1-year Hooli bond, and a short position of $1,000 face value in a 1-year zero-coupon Treasury security priced at $946.934798. Describe the time 0 and time 1 net cash flows of the portfolio if the Hooli bond does not default and if the Hooli bond defaults. Use positive numbers to denote net cash inflows and negative numbers to denote net cash outflows. If Hooli bond does not default, the time 0 net cash flow is $ If Hooli bond does not default, the time 1 net cash flow is $ If Hooli bond does default, the time 0 net cash flow is $ If Hooli bond does default, the time 1 net cash flow is $ (c) 0.0/8.0 points (graded) (c) A credit default option written on the Hooli bond promises that in the event of a default, the option writer will pay the difference between the face value of the Hooli bond and its recovery value, in exchange for an upfront fee. Based on the analysis above and the assumption of no arbitrage, what would be the upfront fee to buy protection on $100,000 face value of the bond? $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts