Question: Problem 2. A European binary (or Digital) option pays $6 if the stock price ends above $55 after 3 months and nothing (pays $0 )

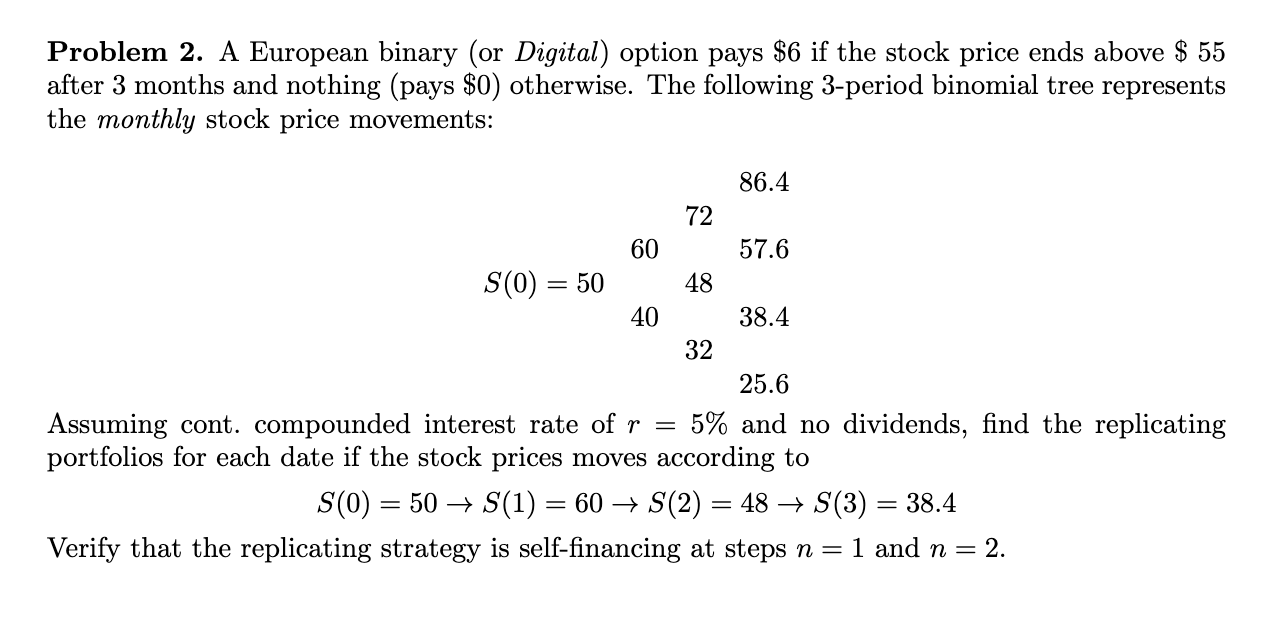

Problem 2. A European binary (or Digital) option pays $6 if the stock price ends above $55 after 3 months and nothing (pays $0 ) otherwise. The following 3-period binomial tree represents the monthly stock price movements: Assuming cont. compounded interest rate of r=5% and no dividends, find the replicating portfolios for each date if the stock prices moves according to S(0)=50S(1)=60S(2)=48S(3)=38.4 Verify that the replicating strategy is self-financing at steps n=1 and n=2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock