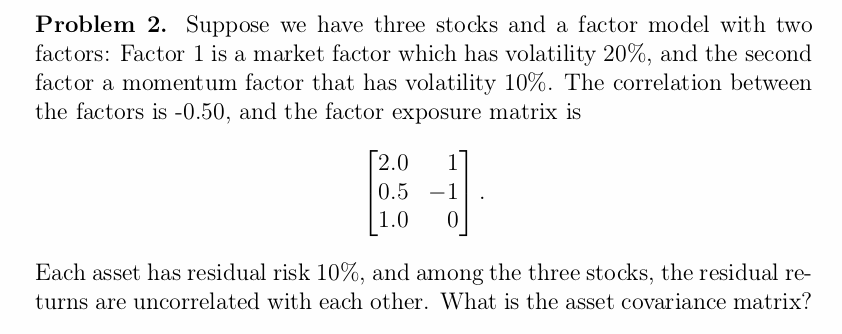

Question: Problem 2. Suppose we have three stocks and a factor model with two factors: Factor l is a market factor which has volatility 20%, and

Problem 2. Suppose we have three stocks and a factor model with two factors: Factor l is a market factor which has volatility 20%, and the second! factor a momentum factor that has volatility 10%. The correlation between the factors is -0.50, and the factor exposure matrix is 2.01 0.51 1.0 0 Each asset has residual risk 10%, and among the three stocks, the residual re- turns are uncorrelated with each other. What is the asset covariance matrix? Problem 2. Suppose we have three stocks and a factor model with two factors: Factor l is a market factor which has volatility 20%, and the second! factor a momentum factor that has volatility 10%. The correlation between the factors is -0.50, and the factor exposure matrix is 2.01 0.51 1.0 0 Each asset has residual risk 10%, and among the three stocks, the residual re- turns are uncorrelated with each other. What is the asset covariance matrix

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts