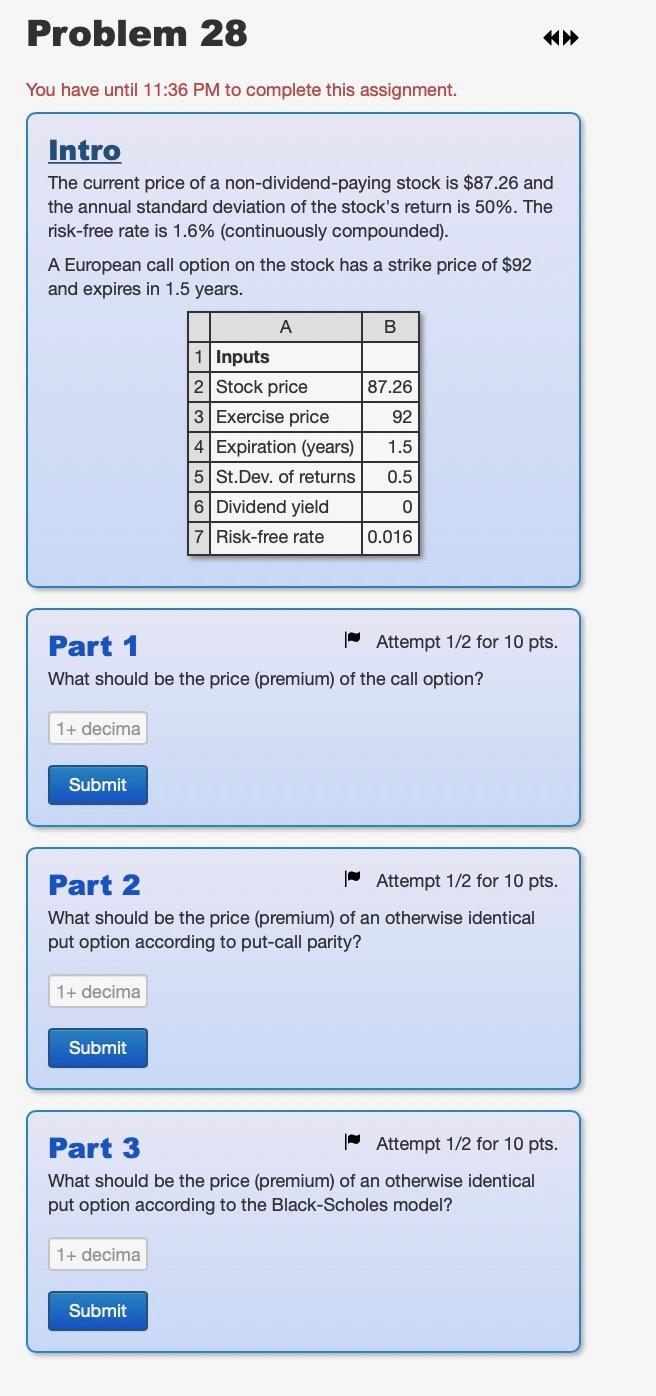

Question: Problem 28 You have until 11:36 PM to complete this assignment. Intro The current price of a non-dividend-paying stock is $87.26 and the annual standard

Problem 28 You have until 11:36 PM to complete this assignment. Intro The current price of a non-dividend-paying stock is $87.26 and the annual standard deviation of the stock's return is 50%. The risk-free rate is 1.6% (continuously compounded). A European call option on the stock has a strike price of $92 and expires in 1.5 years. A B 87.26 1 Inputs 2 Stock price 3 Exercise price 4 Expiration (years) 5 St.Dev. of returns 6 Dividend yield 7 Risk-free rate 92 1.5 0.5 0 0.016 Part 1 Attempt 1/2 for 10 pts. What should be the price (premium) of the call option? 1+ decima Submit Part 2 Attempt 1/2 for 10 pts. What should be the price (premium) of an otherwise identical put option according to put-call parity? 1+ decima Submit Part 3 Attempt 1/2 for 10 pts. What should be the price (premium) of an otherwise identical put option according to the Black-Scholes model? 1+ decima Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts