Question: Problem 3. a) Two European call options on a stock have the same expiration date and strike prices of $50 and $60 and equal prices

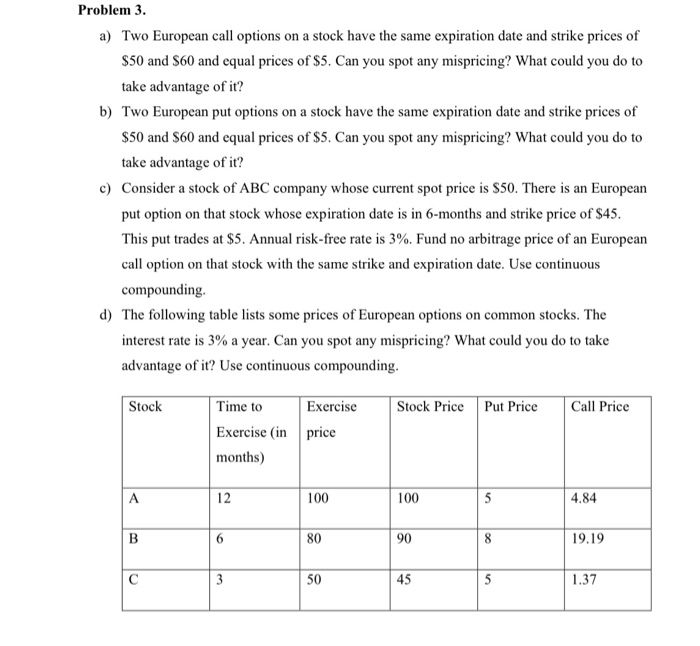

Problem 3. a) Two European call options on a stock have the same expiration date and strike prices of $50 and $60 and equal prices of $5. Can you spot any mispricing? What could you do to take advantage of it? b) Two European put options on a stock have the same expiration date and strike prices of $50 and $60 and equal prices of $5. Can you spot any mispricing? What could you do to take advantage of it? c) Consider a stock of ABC company whose current spot price is $50. There is an European put option on that stock whose expiration date is in 6-months and strike price of $45. This put trades at $5. Annual risk-free rate is 3%. Fund no arbitrage price of an European call option on that stock with the same strike and expiration date. Use continuous compounding d) The following table lists some prices of European options on common stocks. The interest rate is 3% a year. Can you spot any mispricing? What could you do to take advantage of it? Use continuous compounding. Stock Stock Price Put Price Call Price Time to Exercise (in months) Exercise price 100 100 4.84 19.19 1.37

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts