Question: Problem 3-Arizona City Comprehensive Case Study Using the information provided, complete the steps below to complete the Arizona City Comprehensive Case Study. Arizona City General

Problem 3-Arizona City Comprehensive Case Study

Using the information provided, complete the steps below to complete the Arizona City Comprehensive Case Study.

Arizona City General Fund Trial Balance

The trial balance of the General Fund of Arizona City on January 1, 2017, was:

| Debit | Credit | |

| Cash | 1,200,000 | |

| Investments | 485,000 | |

| Taxes Receivable - Delinquent | 165,000 | |

| Allowance for Uncollectible Taxes - Delinquent | 22,000 | |

| Interest and Penalties Receivable | 55,500 | |

| Allowance for Uncollectible Interest and Penalties | 18,500 | |

| Accrued Interest Receivable | 1,500 | |

| Inventory of Materials and Supplies | 50,000 | |

| Accrued Salaries Payable | 53,000 | |

| Vouchers Payable | 110,000 | |

| Deferred Revenues | 98,000 | |

| Due to Internal Services Fund | 9,000 | |

| Fund Balance | 1,646,500 | |

| Totals | 1,957,000 | 1,957,000 |

Arizona City General Fund Budget

The General Fund budget for 2017 was adopted by the city council. The city budgets on the modified accrual basis. Transfers are not budgeted. The adopted budget is presented here:

| Estimated Revenues: | ||

| Taxes | 1,550,000.00 | |

| Interest and Penalties | 16,500.00 | |

| Licenses and permits | 124,000.00 | |

| Fines and forfeitures | 48,000.00 | |

| Intergovernmental grants | 298,000.00 | |

| Investment income | 43,000.00 | |

| Total estimated revenues | 2,079,500.00 | |

| Appropriations: | ||

| General government | 262,000.00 | |

| Public safety | 869,000.00 | |

| Highways and streets | 288,000.00 | |

| Health and sanitation | 216,000.00 | |

| Parks and recreation | 340,000.00 | |

| Total appropriations | 1,975,000.00 | |

| Budgeted excess revenues over appropriations | 104,500.00 |

Arizona City General Fund Transactions - 2017

1. Record the budget. (You may use a single Estimated Revenues account and a single Appropriations account.)

2. Reestablish the encumbrances of $20,000 that were closed at the end of last year.

3. The city levied its general property taxes for the year of $1,560,000. The city estimates that $40,000 of the taxes will prove uncollectible. Record the taxes assuming the city will collect the remaining balance later during the fiscal year.

4. The city collected $1,310,000 of property taxes before the due date for taxes. The remainder of the taxes receivable became delinquent.

5. The city received and vouchered the materials and supplies that were on order from the previous year. The actual cost equaled the estimated cost of these materials and supplies, $20,000. The city records expenditures for materials and supplies when they are consumed. A perpetual inventory system is used.

6 . The city collected $215,000 when investments matured and also collected the following General Fund revenues during the year:

| Fines and forfeitures | $48,400 |

| Unrestricted grants from the state | 346,200 |

| Licenses and permits | 122,400 |

| Interest revenue from investments (including $1,500 accrued at the end of 2016) | 42,000 |

| Total | $559,000 |

7. The city incurred and paid salary expenditures as follows:

| Accrued salaries payable, January 1 | $ 52,000 |

| General government | 180,000 |

| Public safety | 580,000 |

| Highways and streets | 175,000 |

| Health and sanitation | 150,000 |

| Parks and recreation | 240,000 |

| Total | $1,377,000 |

8. The city ordered General Fund materials and supplies as follows:

| General government | $ 10,000 |

| Public safety | 40,000 |

| Highways and streets | 75,000 |

| Health and sanitation | 42,000 |

| Parks and recreation | 40,000 |

| Total | $ 207,000 |

9. Billings were received from the Water and Sewer Enterprise Fund as follows:

| General government | $ 900 |

| Public safety | 13,500 |

| Highways and streets | 3,300 |

| Health and sanitation | 2,900 |

| Parks and recreation | 1,400 |

| Total | $ 22,000 |

10. Equipment was ordered for the following functions:

| General government | $ 35,000 |

| Public safety | 150,000 |

| Highways and streets | 25,000 |

| Health and sanitation | 9,000 |

| Parks and recreation | 60,000 |

| Total | $ 279,000 |

11. The equipment ordered was received (and vouchers approved) as follows:

|

| Estimated Cost | Actual Costs |

|

|

| |

| General government | $ 35,000 | $ 35,000 |

| Public safety | 134,000 | 135,000 |

| Highways and streets | 25,300 | 25,300 |

| Health and sanitation | 8,900 | 8,900 |

| Parks and recreation | 60,000 | 60,000 |

| Totals | $263,200 | $ 264,200 |

12. Billings were received from the Central Communications Network Internal Service Fund for communications services used by general government agencies and departments as follows:

| General government | $ 17,000 |

| Public safety | 15,000 |

| Highways and streets | 3,500 |

| Health and sanitation | 6,600 |

| Parks and recreation | 13,900 |

| Total | $ 56,000 |

13. A total of $61,000 was paid on the amounts owed to the Central Communications Network Internal Service Fund.

14. Other unencumbered expenditures incurred during the year were vouchered as follows:

| General government | $ 11,500 |

| Public safety | 41,200 |

| Total | $ 52,700 |

15. The General Fund loaned $500,000 to the Addiction Prevention Special Revenue Fund to provide working capital for that fund. The loan is to be repaid within a year.

16. The General Fund transferred resources to other funds as follows:

| Addiction Prevention Special Revenue Fund | $ 70,000 |

| Parks and Recreation Capital Projects Fund | 200,000 |

| Bridge Capital Projects Fund | 69,000 |

| Refunding Debt Service Fund | 730,000 |

| Total | $1,069,000 |

17. The General Fund received a transfer of $100,000 from the Water and Sewer Enterprise Fund.

18. Accrued salaries and wages for General Fund employees at December 31 were as follows:

| General government | $ 1,700 |

| Public safety | 5,800 |

| Highways and streets | 1,700 |

| Health and sanitation | 1,500 |

| Parks and recreation | 2,300 |

| Total | $ 13,000 |

Required Steps

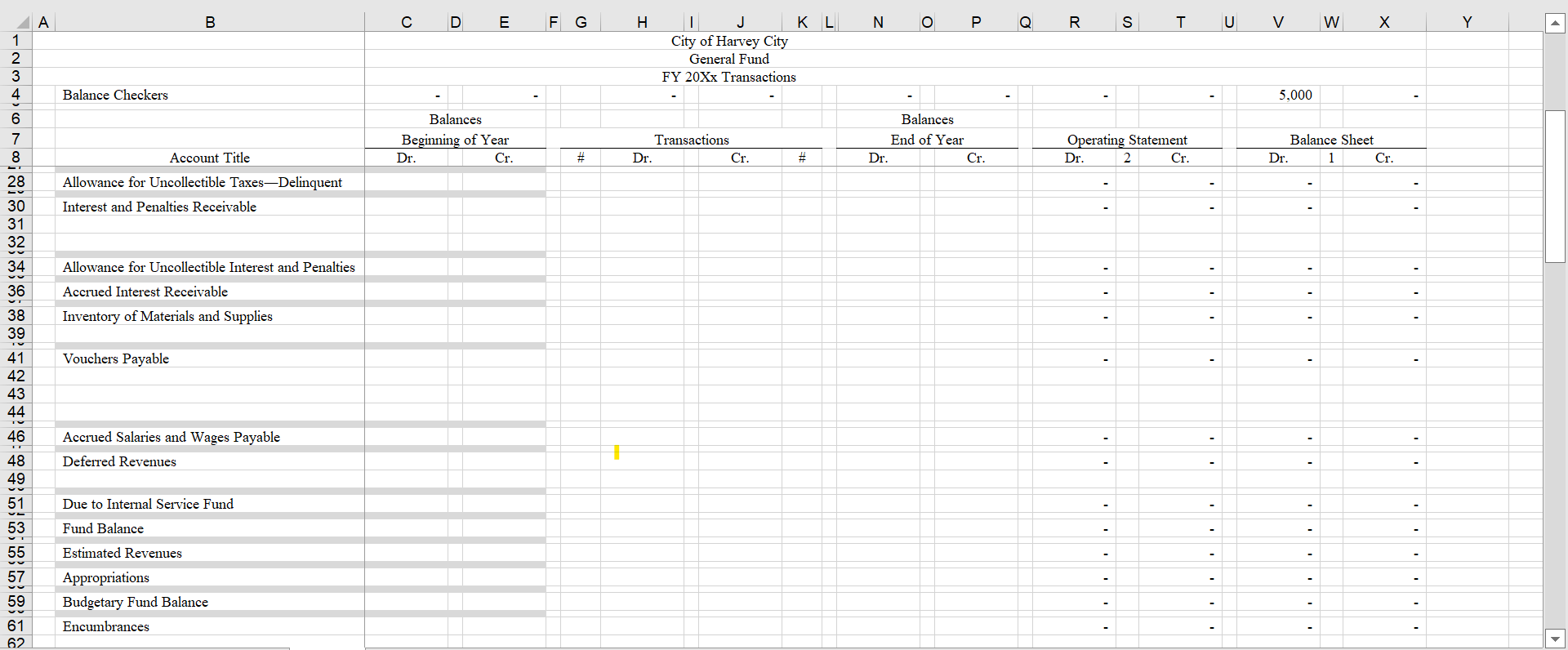

1. Enter the beginning (January 1, 2017) trial balance of the General Fund of Arizona City in a General Fund worksheet.

The first column should be used for account titles.

Columns 2 and 3 should be the debit and credit columns, respectively, for the beginning trial balance of the General Fund.

Column 4 of the worksheet should be a reference column to tie the journal entry debits to the transaction number in this problem.

Column 7 of the worksheet should be a reference column to tie the journal entry credits to the transaction number in this problem.

Columns 8 and 9 are for the preclosing trial balance of the Arizona City General Fund.

Columns 10 and 11 are to be used to close the nonbudgetary accounts of Arizona City. These columns also will contain all balances that are to be reported in the General Fund statement of revenues, expenditures, and changes in fund balances.

Columns 12 and 13 are to be used for the post-closing trial balance (balance sheet data). All assets, deferred outflow, liability, deferred inflow, and fund balance amounts should be entered here from the trial balance columns.

The differences between the closing entry columns and the balance sheet columns should be equal to each other and to the net change in fund balances of the General Fund. This amount should be entered in the smaller of the closing entry columns and the smaller of the balance sheet columns. (If the closing entry debit column is smaller, the balance sheet credit column should be smallerand vice versa.)

2. Enter the effects of the provided transactions and events in the appropriate columns of the worksheet.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts