Question: Problem 3-Duration Gap (12 pts) Suppose you are an executive at Dedham Savings and Loan. This institution issues mortgages and small business loans. The bank

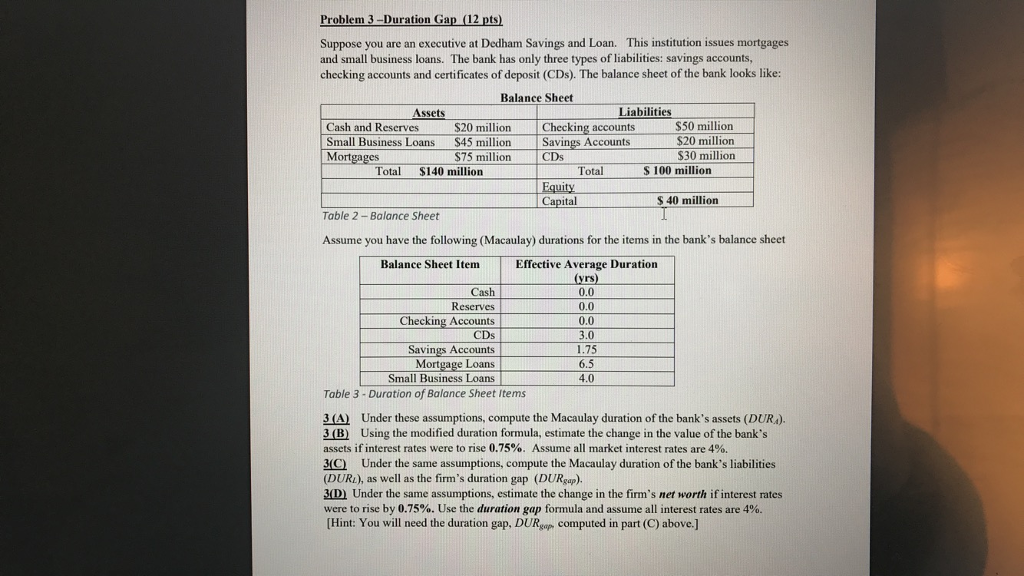

Problem 3-Duration Gap (12 pts) Suppose you are an executive at Dedham Savings and Loan. This institution issues mortgages and small business loans. The bank has only three types of liabilities: savings accounts, checking accounts and certificates of deposit (CDs). The balance sheet of the bank looks like: Balance Sheet Assets Liabilities Cash and Reserves Small Business Loans $45 million Savings Mort S20 millionChecking accounts $75 million CDs $50 million $20 million $30 million Accounts Tota $140 million Total S 100 million Equity $ 40 million Table 2 -Balance Sheet Assume you have the following (Macaulay) durations for the items in the bank's balance sheet Effective Average Duration (yrs) 0.0 0.0 0.0 Balance Sheet Item Cash Reserves Checking Accounts CDs Savings Accounts Mortgage Loans 1.75 6.5 Small Business Loans4.0 Table 3 - Duration of Balance Sheet Items 3(A) Under these assumptions, compute the Macaulay duration of the bank's assets (DURA) 3(B) Using the modified duration formula, estimate the change in the value of the bank's assets if interest rates were to rise 0.75%. Assume all market interest rates are 4%. 3(C Under the same assumptions, compute the Macaulay duration of the bank's liabilities (DURL), as well as the firm's duration gap (DURgap) 3D) Under the same assumptions, estimate the change in the firm's net worth if interest rates were to rise by 0.75%. Use the duration gap formula and assume all interest rates are 4%. Hint: You will need the duration gap, DURgop computed in part (C) above.]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts