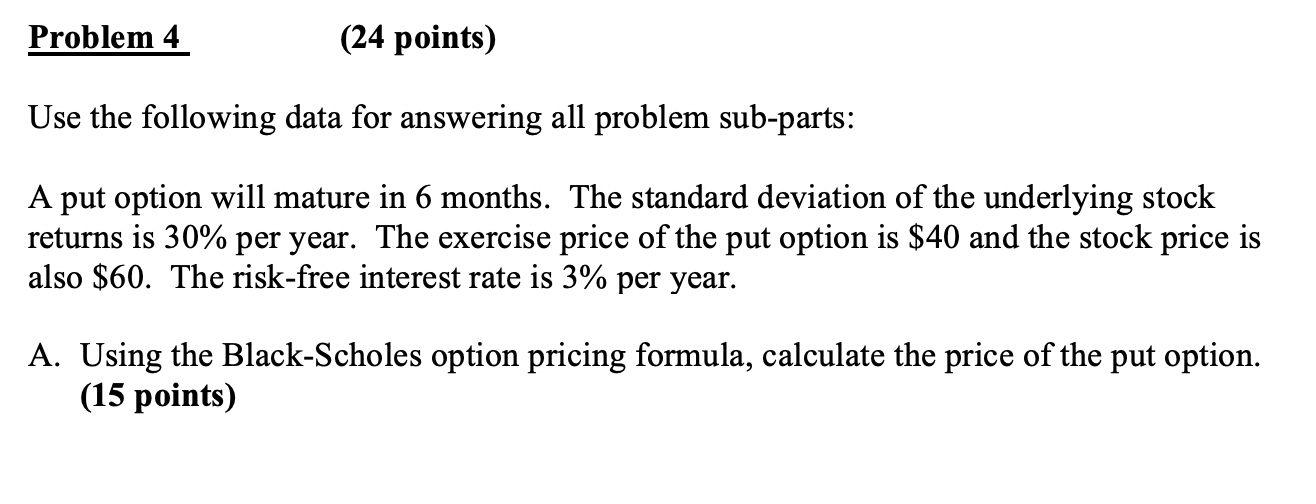

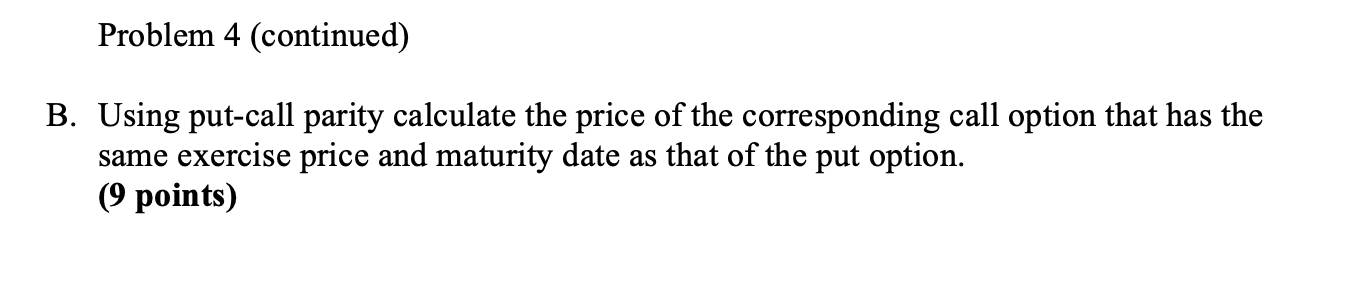

Question: Problem 4 (24 points) Use the following data for answering all problem sub-parts: A put option will mature in 6 months. The standard deviation of

Problem 4 (24 points) Use the following data for answering all problem sub-parts: A put option will mature in 6 months. The standard deviation of the underlying stock returns is 30% per year. The exercise price of the put option is $40 and the stock price is also $60. The risk-free interest rate is 3% per year. A. Using the Black-Scholes option pricing formula, calculate the price of the put option. (15 points) Problem 4 (24 points) Use the following data for answering all problem sub-parts: A put option will mature in 6 months. The standard deviation of the underlying stock returns is 30% per year. The exercise price of the put option is $40 and the stock price is also $60. The risk-free interest rate is 3% per year. A. Using the Black-Scholes option pricing formula, calculate the price of the put option. (15 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts