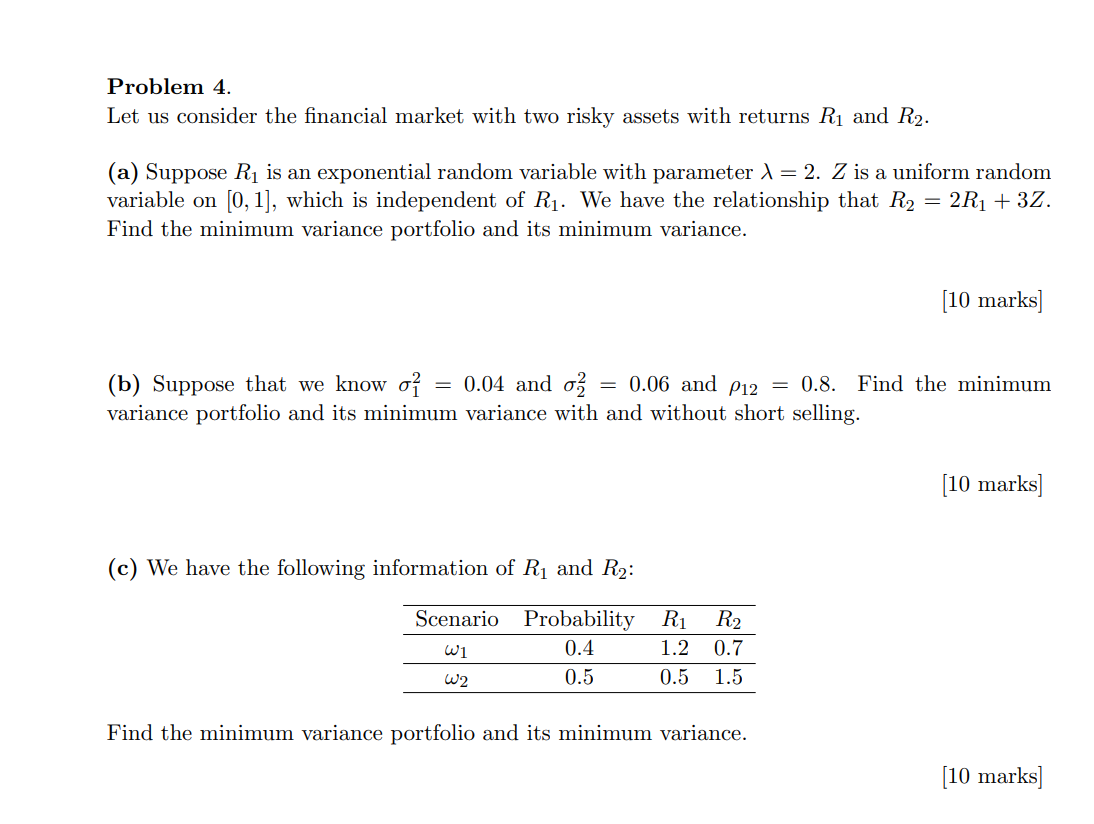

Question: Problem 4. Let us consider the financial market with two risky assets with returns R1 and R2. (a) Suppose R1 is an exponential random variable

Problem 4. Let us consider the financial market with two risky assets with returns R1 and R2. (a) Suppose R1 is an exponential random variable with parameter 1 = 2. Z is a uniform random variable on [0, 1], which is independent of R1. We have the relationship that R2 = 2R1 + 32. Find the minimum variance portfolio and its minimum variance. [10 marks] (b) Suppose that we know oi = 0.04 and o = 0.06 and P12 = 0.8. Find the minimum variance portfolio and its minimum variance with and without short selling. [10 marks] (c) We have the following information of R and R2: Scenario Probability 0.4 W2 0.5 R1 1.2 R2 0.7 1 0.5 1.5 Find the minimum variance portfolio and its minimum variance. [10 marks] Problem 4. Let us consider the financial market with two risky assets with returns R1 and R2. (a) Suppose R1 is an exponential random variable with parameter 1 = 2. Z is a uniform random variable on [0, 1], which is independent of R1. We have the relationship that R2 = 2R1 + 32. Find the minimum variance portfolio and its minimum variance. [10 marks] (b) Suppose that we know oi = 0.04 and o = 0.06 and P12 = 0.8. Find the minimum variance portfolio and its minimum variance with and without short selling. [10 marks] (c) We have the following information of R and R2: Scenario Probability 0.4 W2 0.5 R1 1.2 R2 0.7 1 0.5 1.5 Find the minimum variance portfolio and its minimum variance. [10 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts