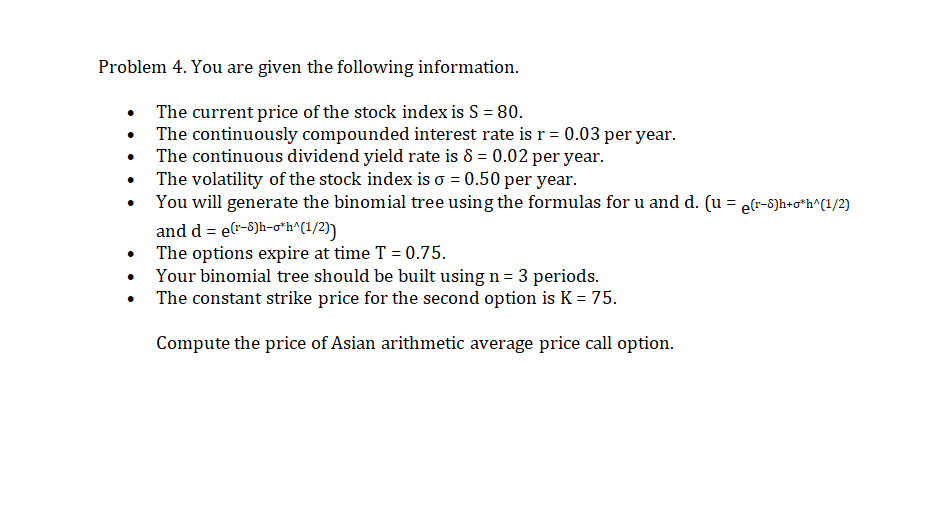

Question: Problem 4. You are given the following information. . The current price ofthe stock index is S = 80. . The continuously compounded interest rate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts